COMMITLY setzt als Rahmen (Template) für die Liquiditätsplanung die sogenannte direkte Cash Flow Ermittlung ein. Im Finanzjargon bedeutet das, dass zahlungswirksame Erträge mit den zahlungswirksamen Aufwendungen saldiert werden. Auf gut Deutsch heißt das, dass wir den verfügbaren Cash Flow oder auch Free Cash Flow als Differenz zwischen den Zahlungseingängen und den -ausgängen auf den mit COMMITLY verbundenen Konten errechnen.

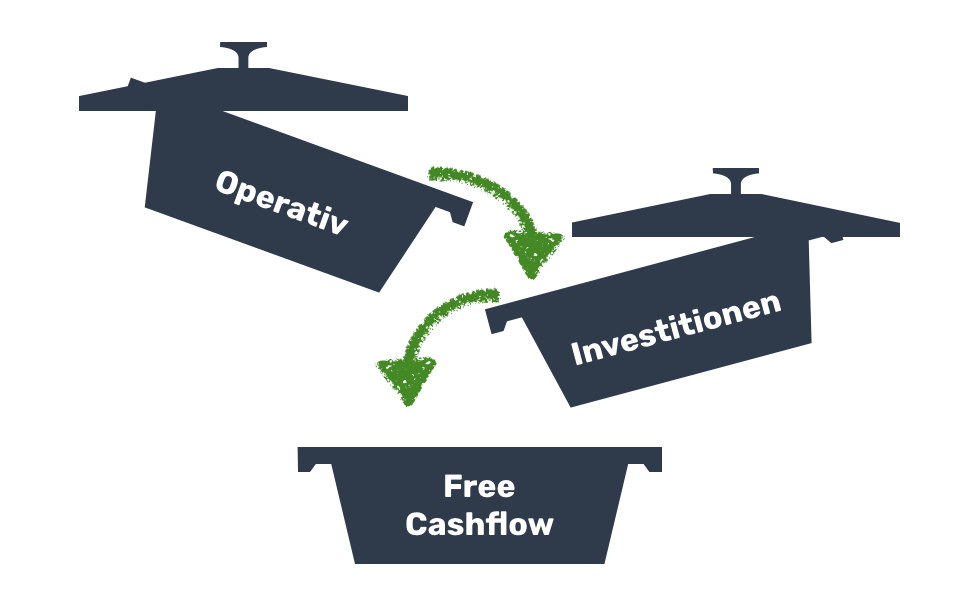

Das Schema der direkten Cashflow Ermittlung

Bei der Berechnung werden die Ein- und Ausgänge in 3 Gruppen unterteilt:

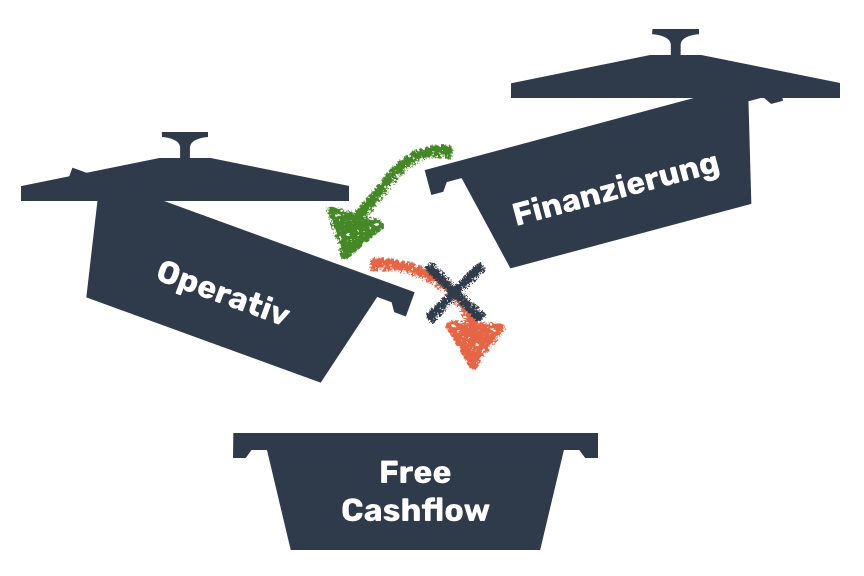

A – Operativer Cash Flow:

Der operative Cash Flow gibt an, ob dein Unternehmen in der Lage ist, sich selbst zu finanzieren. Wenn die laufenden Einnahmen (Zahlungseingänge) in einem bestimmten Zeitraum höher sind als deine laufenden Ausgaben (Zahlungsausgänge), ist alles im grünen Bereich. Weiter so!

B – Cash Flow aus der Investitionstätigkeit

Dieser Topf gibt an, ob du für dein Unternehmen Investitionen getätigt hast oder Vermögensgegenstände gekauft hast. Wenn dein Cash Flow aus der laufenden Geschäftstätigkeit positiv ist, d.h. Geld vorhanden ist bzw. übrig bleibt, hast du die Möglichkeit, Investitionen zu tätigen, also z.B. einen neuen Arbeitsplatz inkl. PC zu kaufen.

C – Cash Flow aus der Finanzierungstätigkeit

Dieser gibt an, ob dein Unternehmen Kredite aufgenommen oder getilgt hat oder Auszahlungen an die Gesellschafter vorgenommen hat (Dividenden) bzw. Einzahlungen von Gesellschafter erhalten hat. Eine Entnahme über den Unternehmerlohn hinaus fällt auch in diese Kategorie. Wenn die operative Geschäftstätigkeit zu wenig Cash Flow liefert, kannst du auch aus diesem Topf, z.B. mit deinem Unternehmenskredit, Investitionen tätigen.

Warum sind diese “Töpfe” aber eigentlich so wichtig?

Weil sie zusammen die Finanzkraft deines Unternehmens bestens abbilden. Wir haben in unserem Beispiel den Best Case dargestellt: Deine Geschäfte laufen so gut, dass du aus deinen laufenden Einnahmen einen Überschuss erzielst, investieren kannst und dir sogar noch etwas überbleibt. Das was übrig bleibt ist dann übrigens der „Free Cash Flow“.

Ein positiver frei verfügbarer Cashflow / Free Cash Flow

Der positive „Free Cash Flow“ steht dir zur freien Verfügung. Das heißt, du hast alle laufenden Ausgaben gedeckt, hast Investitionen getätigt und es ist noch etwas übergeblieben. Gratulation!

Was tut man am besten mit dem Free Cash Flow?

- Einen Liquiditätspuffer als Vorsorge aufbauen

- In neue Projekte oder etwa neue Mitarbeiter investieren

- Kredite vorzeitig zurückzahlen

- Gewinne entnehmen

- …

Was tun bei einem negativen operativen Cashflow?

Doch was ist, wenn dein operativer Cashflow negativ ist, das heißt, wenn deine Ausgaben (Zahlungsausgänge) höher sind als die Einnahmen (Zahlungseingänge)?

Erstens: Nicht verzweifeln! Zweitens: Halte dir vor Augen, dass du nicht alleine mit diesem Problem bist! Beinahe jeder Unternehmer kennt diese Situation: In einem Monat haben sich die Zahlungseingänge verspätet und nicht alle Ausgaben können reibungslos gezahlt werden.

Glücklich, wer sich aus der Vorperioden einen Liquiditätspuffer aufgebaut hat. Dann handelt es sich nur um einen temporären Liquiditätsengpaß. Wenn nicht, hilft nur der Cashflow aus Finanzierung – also der Griff in die eigenen Taschen oder der Gang zum Investor oder der Bank.

Welche Maßnahmen können also getroffen werden?

- Prüfen, ob Investitionen nach hinten geschoben werden können

- Wenn es verwertbares Anlagevermögen gibt, kann evtl. auch eine Veräußerung (Devestition) geprüft werden.

- Finanzierung – gibt es Zugriff auf Darlehen, Förderungen, frisches Eigenkapital

- Ebenfalls in den Bereich der Finanzieurng fällt der Verzicht auf Entnahmen

Stellt COMMITLY damit ausschließlich auf die Bankkonten ab?

Die kurze Antwort ist: Ja! Und was ist mit den Daten aus der Buchhaltung? Hauptaufgabe der Buchhaltung ist die gesetzlich korrekte Abbildung der Vergangenheit. Die Planung betrifft die Zukunft, hat keine gesetzlichen Vorgaben UND man kann auch nichts „kaputt“ machen. Das ist ein wichtiger Aspekt, der auch von unseren Kunden angeführt wird. Der bekannte Investor Fred Wilson hat in seinem Blog auch einen anderen sehr wichtigen Aspekt beschrieben – unterschiedliche Typen. Die Finanzfunktion: Rückblick und Blick nach vorne

“Meiner Erfahrung nach sind die Menschen, die in der Rückschau-Funktion stark sind, oft nicht in der Vorwärts-Funktion stark. Möglicherweise benötigen Sie verschiedene Personen, um diese Rollen zu übernehmen. In einem großen Unternehmen gibt es ganz unterschiedliche Abteilungen, die diese Funktionen übernehmen. Es gibt eine Buchhaltungsabteilung und eine Finanzplanungsabteilung (oft FP&A genannt).”

Ist COMMITLY damit nur für Einahmen Überschuss Rechner sinnvoll?

Nein! Unternehmen mit doppelter Buchführung haben aus der Buchhaltung heraus gerade limitierten Einblick in ihren Cash Flow. Das führt dann oft dazu, dass die indirekte Methode zur Ermittlung des Cash Flows herangezogen wird. Aufsatzpunkt dabei ist dann das Periodenergebnis und es werden sogenannte non-cash items, also nicht zahlungswirksame Erlöse und Aufwände wie z.B. Abschreibungen herausgerechnet. Zusätzlich hat man noch Themen mit Periodenabgrenzungen. Die indirekte Ableitung ist aber so kompliziert, dass das in der Regel vom Steuerberater gemacht wird, mit entsprechender zeitlicher Verzögerung. ABER: Mir hat mal ein großer Steuerberater gesagt, dass nur 10% SEINER Mitarbeiter eine Ahnung haben, wie das geht.

Ist die indirekte Ermittlung nicht doch besser für größere Unternehmen?

Die direkte Ermittlung, wie von COMMITLY eingesetzt, ist super einfach und deckt alle Szenarien und auch Buchhaltungsformen UND auch Unternehmensgrößen ab. Das „Verbindungsstück“ wenn man so will, ist der Cashbestand bzw. der Kontostand der Banken. Das ist auch das besondere bei COMMITLY. In der Praxis haben wir selten (eigentlich nie) Liquiditätsplanungen (und auch Cash Flow Berichte) in Excel gesehen, die 1:1 mit der Buchhaltung abstimmbar waren. COMMITLY gewährleistet das.

Warum? Weil am Ende einer Periode die wichtigste Basis eines Steuerberaters (egal ob EÜR oder doppelte Buchhaltung) die Abstimmung mit dem Bankkonto ist. Und das ist automatisch in COMMITLY gewährleistet.