In this article you will find everything you need to know about Cash flow planning. What is behind the word Cash flow plan, how to create an Cash flow planning , what templates are available, examples of planning, etc.

Cash position and Cash flow planning have been with me at all stages of my career for 20 years now. From finance assistant to CFO, with the responsibility to ensure the Cash position of the company. If something is missing or a question is not answered, please let me know directly at juergen@commitly.com!

Why Cash flow planning?

Nothing compares to the importance of Cash position in small and medium-sized enterprises. Because the options for action in the event of bottlenecks in the area of Cash position in small companies are severely limited compared to large companies. And unfortunately, far too often the need for action is only recognized very late.

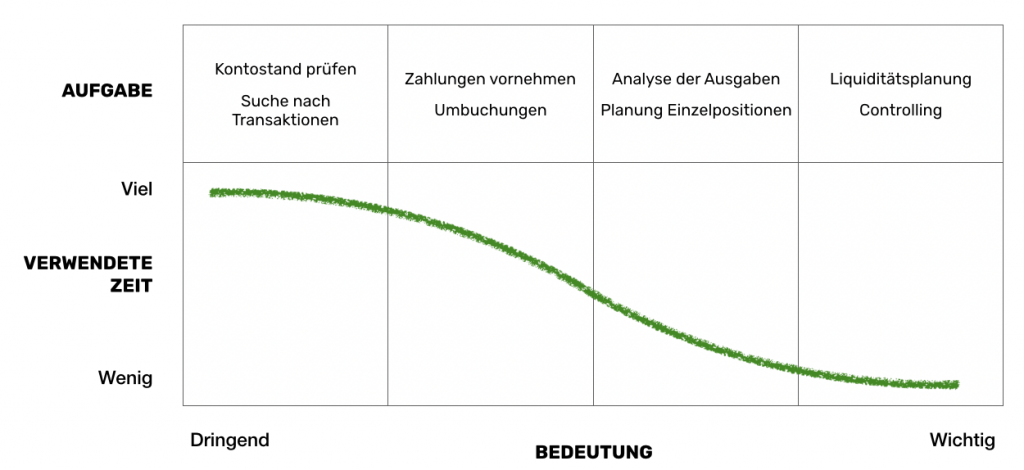

Who does not know it? Urgent vs. Important!

Figure: Imbalance of urgent vs. important tasks in the area of Cash position

As a rule, the options for action to overcome a liquidity bottleneck are then limited to three things:

- external financing by the (house) bank,

- Waiver of withdrawals

- Financing by owners

Wait a minute! And what about the utilisation of payment terms with suppliers or possibilities of advance payments from customers? When thinking about these things, it is urgent to check the basic solvency of the company. But I will come to that later.

The Cash flow plan

The Cash flow plan or cash flow statement determines the future cash flows of a company, i.e. compares the expected income with the expected expenditure in a systematic form. The systematic form refers to the planning template used. The template depends on the requirements of the company or entrepreneur. The expected cash flows, i.e. income and expenditure, can be defined differently.

- In the case of transactions that have already taken place, these are referred to as deposits or withdrawals.

- In the actual definition, additional "open items" are understood, i.e. those already existing outgoing or incoming invoices that have not yet been paid.

- In an extended definition used in planning, this is also expected income and expenditure over a longer period of time without underlying invoices. Often these expected receipts and payments are derived from a financial plan.

Receipts and payments as well as expenditures and disbursements are often used synonymously. However, this is also the time to clarify some important conceptual differences.

So what is a cash flow statement?

The cash flow statement, a synonym for Cash flow planning, determines the future cash flows of a company and compares them in a systematic form.

Cash flows: receipts vs. revenues or payments vs. expenses

In the case of payment flows, there is often a mixture of different terms. Revenues / expenses are terms from double-entry accounting. For revenues or expenses, it is irrelevant whether an incoming payment or a payment has already been made.

Deposits/withdrawals are terms from Cash flow planning and are very easy to identify: Has there been a movement on the account? If so, then this is a deposit or withdrawal.

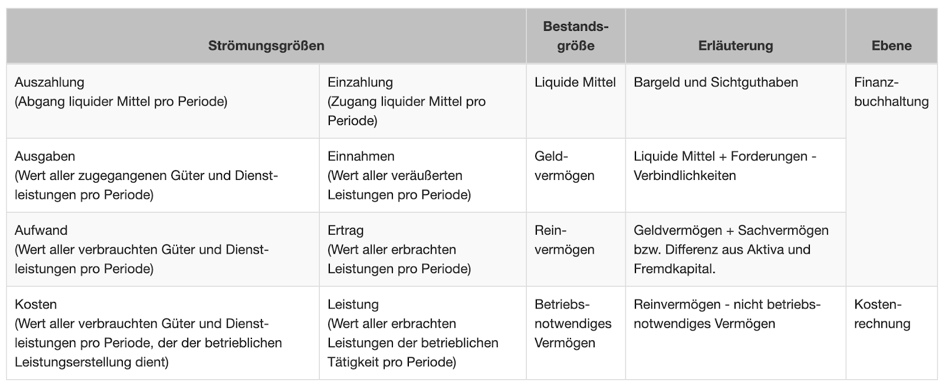

All terms can be assigned to the subject area of financial accounting. The main difference is the result obtained. Even the search with Google is not trivial.

We have found a very good presentation on Rechnungswesen-info.de:

Fig: Definitions of terms in financial accounting (and cost accounting)

This table also mentions the terms expenses and income. These are broader technical terms in Cash flow planning and, in addition to the actual transactions, also include open items, i.e. expenses or income that are not yet payments or receipts.

Objective of the Cash flow plan

The purpose of Cash flow plan is to show the future available liquid funds of a company, i.e. the liquidity position on a specific day. In other words: How much money will be available to the company in 3 weeks, 3 months, 12 months, on a specific day, etc. Classic questions that should be answered with the help of Cash flow plan are

- Can I afford an additional employee?

- Can I pre-finance a big project? (Do I have the "breath" for it?)

- Can I repay a loan due on day xx. or do I have to refinance?

The overriding objective is to ensure and monitor solvency at all times. This is one of the most important tasks of an entrepreneur, cannot be delegated and, if ignored, even has consequences under criminal law (key words: going concern forecast, negligence, delaying insolvency).

I would even go that far: A financial plan is optional, but Cash flow planning is mandatory.

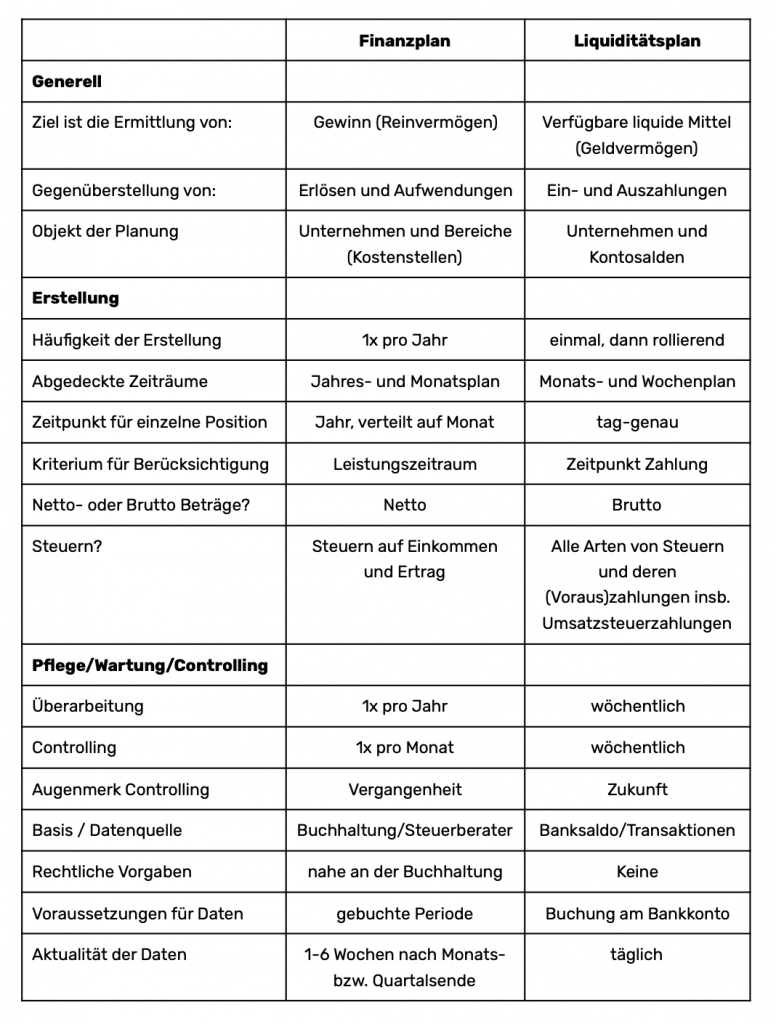

Stop! Finance plan again? Before we go any further, we should first define some important terms or work out the differences.

Financial plan vs. Cash flow plan

The financial plan of a company compares the expected revenues of a company with the expected expenses in a period and aims to determine the profit. The core of a financial plan is a planned profit and loss account or planned P&L for a specific period, usually a business year. The plan P&L is often accompanied by subsidiary calculations or detailed planning, such as turnover planning, an investment calculation, financing planning and personnel planning.

In larger companies, the finance plan is also divided into (business) areas or cost centres. In a more or less complex form, there may also be a subsidiary calculation for taxes on income. Actually, the budgeted balance sheet would also be part of a financial plan. In practice, however, it is often neglected and replaced by the above-mentioned subsidiary calculations.

There is a good reason for this. The financial plan maps the accounting of a period. The preparation of a budgeted balance sheet would therefore be equivalent to the preparation of financial statements (by a tax advisor). And since accounting is a closed cycle and many financial plans are made in Excel, the Excel planner's greatest enemy arises with a budgeted balance sheet: circular reference!

This necessary attention to detail and complexity have led in practice to the fact that the preparation of the budgeted balance sheet is often dispensed with.

The financial plan is always prepared at the time of foundation and then at least annually (period). In larger companies and groups, financial planning is done several times a year in planning cycles. Our friends at Billomat - those who love accounting - have written a short article on the subject of the financial plan that is well worth reading:

So, what are the differences between a finance plan and a cash flow plan?

And on it goes ...

Business plan vs. finance plan

The business plan is, so to speak, the broadest term in the field of planning. A fully comprehensive business plan is usually drawn up when a company is founded and has two groups of recipients:

- internal - the founding team

- External - funding agencies, investors

A business plan also consists of a variety of qualitative and quantitative elements:

- Executive Summary

- Personal data of the founders

- Presentation of the product or service idea

- Customer description and marketing planning

- Description of the competition

- Presentation of purchasing and production planning

- Presentation of the choice of location and legal form

- Opportunities and risks

- Financial planning

- Appendix

- etc.

Fuer-gruender.de has provided a very comprehensive description in this article: Business Plan Introduction

A great, simple method to define all components holistically is also provided by the Business Model Canvas:

Click here for the official website https://www.strategyzer.com/

Cash flow plan vs. cash flow statement

For the sake of completeness, we should actually also add vs. cash flow statement. Essentially, all three terms describe the same thing, namely Cash flow plan. However, the term cash flow statement is generally used in retrospect. For large companies, the cash flow statement is part of the annual or consolidated financial statements.

Another peculiarity compared to Cash flow plan is that the cash flow statement usually uses the indirect method to determine cash and cash equivalents. Instead of comparing income directly with expenditure, the differences between assets and liabilities are used to determine the amount of cash and cash equivalents.

As a "financier", I'm now going into raptures about the various definitions of indirect determination, but I'd better leave that alone at this point. Because the cash flow statement is an ideal transition to the next topic: the template for a Cash flow planning.

Templates for a Cash flow plan

The ideal template is the cash flow statement. Why? A template for a Cash flow plan should (1) contain all elements of financial planning, (2) be transferable to accounting and (3) enable reconciliation with the bank account. In addition, the requirements with regard to time-based evaluations and data maintenance must be taken into account.

For example, when US investors say that the Cash flow planning or the cash forecast model should be based on the income statement, supplemented by balance sheet items, they are talking precisely about this cash flow statement.

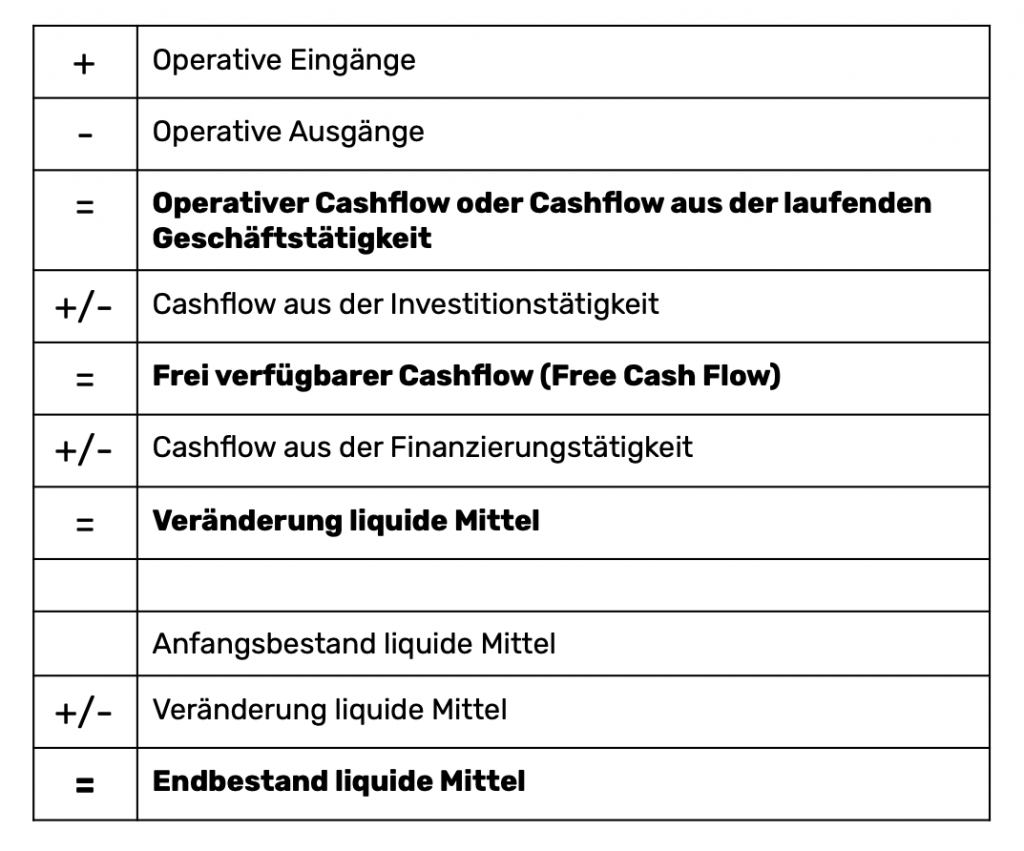

Cash flow scheme (cash flow statement)

We now know from the financial plan that it includes a planned income statement and subsidiary statements. We have also established that Cash flow plan and cash flow statement are synonyms. This means that the ideal template for a Cash flow plan is the cash flow statement template. To be more specific, the method of directly determining the cash flow statement or cash flow statement. This is also the reason why COMMITLY uses this method.

Let us briefly examine this hypothesis: The cash flow from operating activities compares the operating income and expenses, essentially in the scheme of a profit and loss statement. In the area of income, the assumptions of the ancillary calculation of turnover planning flow in, in the area of expenditure, personnel planning. The cash flow from investment reflects the investment planning, the cash flow from financing the financing planning.

Since Cash flow planning contains all incoming and outgoing payments, the cash and cash equivalents at the end of a period must also match the figures in the accounts. This essentially results in the following scheme:

A more detailed description of the scheme including categories can be found here.

This leaves the issue of requirements for time-based evaluation. In Cash flow planning in particular, there is often a requirement for planning on a weekly basis. Ideally, it is therefore possible to choose between different timelines.

Templates mainly for the surplus income statement

In Austria, by the way, the revenue surplus statement is referred to as a revenue expenditure statement. If you google template Cash flow planning you get over 69,000 results in 0.38 seconds. That's great!

If you take a closer look at the results of the search, you will quickly realise that it is not that easy to find the right template. Here are links to some free examples:

- https://www.ihk-schleswig-holstein.de/starthilfe/existenzgruendung/gruendungskonzept/liquiditaetsplan/1368412

- https://heenemann.de/downloads/

- https://www.constanze-elter.de › 2018/03 › Kap-5_Liquiditaetsplan2

One template that I would like to highlight is the Kfw - Bank mit Verantwortung template. As part of the funding offer for domestic companies, there is also a checklist-4 Cash flow plan. This is an editable pdf.

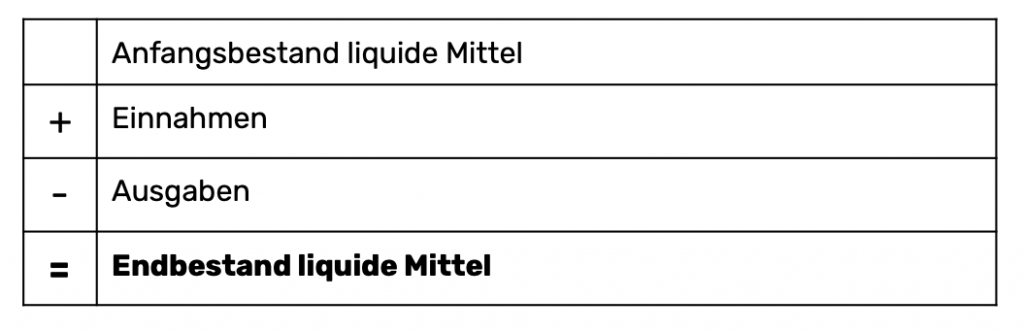

Essentially, these examples always use a scheme:

The disadvantage of this approach is that income and expenditure are not divided into the groups operational, investment, financing. This is important because the groups also reflect the possibilities of influence. Investments - can often be "pushed", i.e. shifted backwards in time. Financing, especially when it comes to withdrawals, can also be controlled.

Furthermore, this presentation does NOT allow statements about the monthly average income or expenditure, as these are usually made WITHOUT effects such as investments or financing. All templates have one thing in common. They are aimed at very small entrepreneurs and, in our opinion, mix up essential components.

The separation into operative incoming and outgoing payments as well as the areas of investment and financing discussed above has great advantages. The separation makes it possible to make a statement about regularly recurring cash inflows and outflows as well as about trends. Usually, jumps in incoming and outgoing payments indicate financing and investment activities.

We often hear in our conversations during onboardings: The amount of exits this month can't be right!

This is almost always the indication that, for example, a loan repayment, an investment or even a withdrawal took place in this month. The use of the cash flow statement scheme remedies this. By separating these three areas, a normalisation takes place statistically, which is the prerequisite for being able to make trend statements at all.

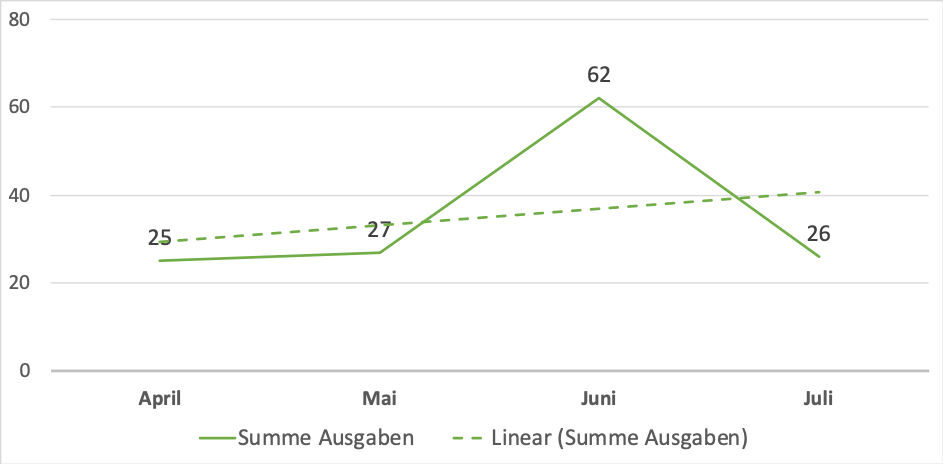

Here is a highly simplified example of this situation:

You know that your expenditure per month is +/- 25. In a graph you now see a value of 62 last June, but in the external view without further information this would result in an average expenditure of 40.

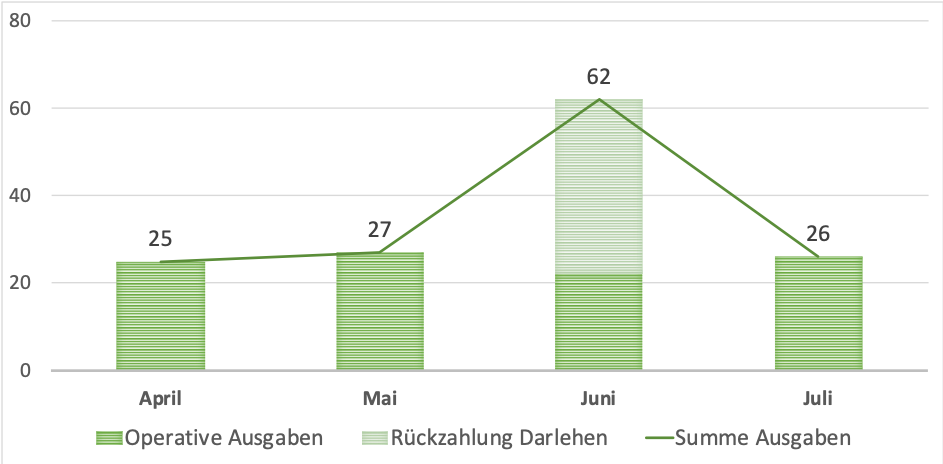

The mere summation of expenditures can therefore have a distorting effect. If we now split the expenditure into the groups operational and financing, the following picture emerges:

At first glance, it can be seen that expenditure increased in June due to the repayment of a loan and that operating expenditure is within the expected range.

Templates within the framework of a continuation forecast

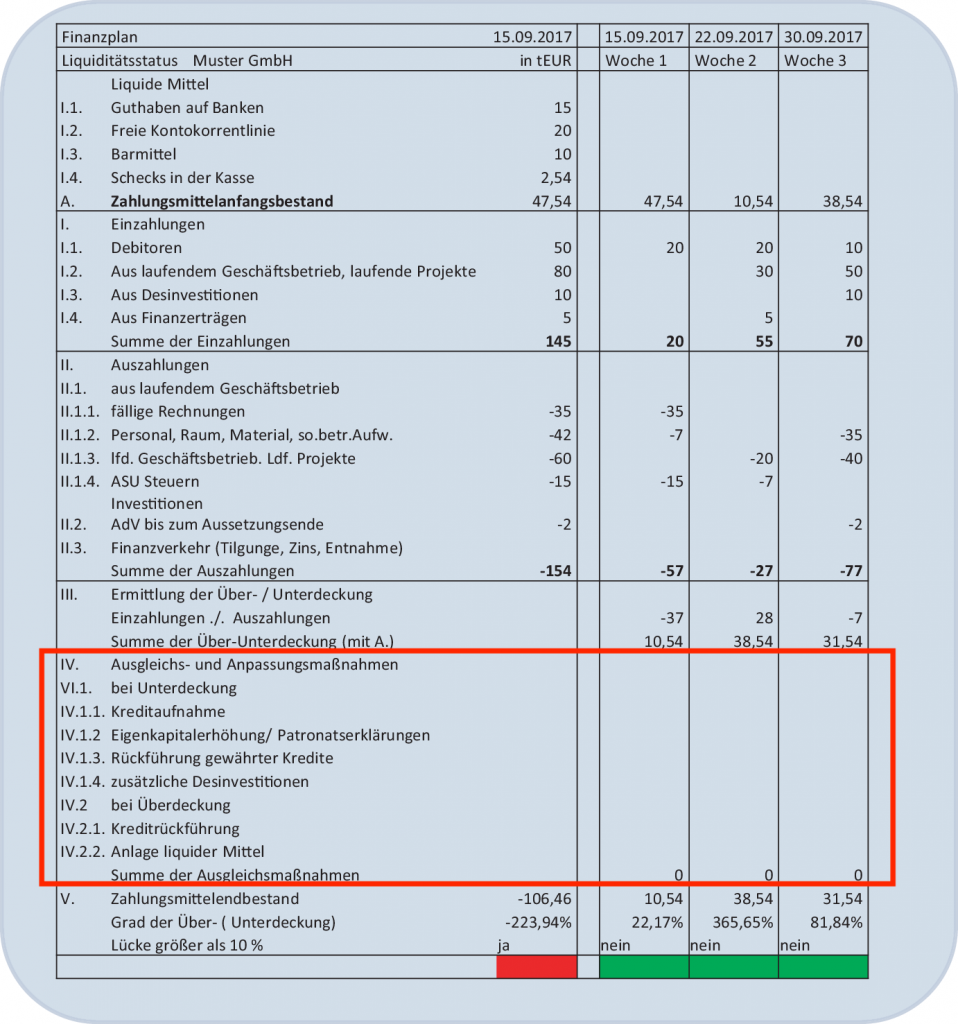

A special case for Cash flow planning is in the event of imminent insolvency. As mentioned at the beginning, the ongoing monitoring of Cash position is one of the most important tasks of the entrepreneur or managing director. The going concern forecast is described and regulated in IDW S 11, although IDW S 11 itself does not provide a specific template.

In the example, the template of Cash flow plan is expanded to include compensation or adjustment measures. This shows which operational, investment or financing measures the entrepreneur takes to eliminate the liquidity shortfall (area outlined in red). Unfortunately, however, this is not clearly structured.

Source: Praxishandbuch Sanierung im Mittelstand - Chapter: The corporate crisis: types, causes, stages and analysis, Springer

I have deliberately written this in a rather complicated way to underline once again the importance of the cash flow diagram as a template with its subdivision into operating, investing and financing.

What is Cash flow planning?

Cash flow planning is the activity of creating a Cash flow plan. It is therefore about filling a planning template with expected cash flows as receipts or payments. The terms Cash flow plan and Cash flow planning are often used interchangeably.

Basis of the Cash flow planning

The most important basis for every Cash flow planning is the level of available funds, i.e. the liquidity position. Available funds are usually the existing credit balance in bank accounts (bank balances) and any unused credit line. This means that the bank account and the current actual figures are at the center of Cash flow planning and not the bookkeeping.

Why not bookkeeping? Because the main task of bookkeeping is the proper mapping of the company's business transactions in a period and usually the booking of business transactions happens relatively late. Thus, in many cases, the basis or control of the bookings is the bank's turnover list.

Creation of the Cash flow planning

The activity of the Cash flow planning can be time

- in the initial creation and then

- into ongoing maintenance or rolling Cash flow planning .

How often do you do a Cash flow planning?

Cash position is a time value and means being able to meet your payment obligations at any time, i.e. every day. It is about the development of liquidity. The preparation of liquidity planning is therefore heavily dependent on the amount of cash and cash equivalents (usually bank balances and cash in hand) in relation to the expected outflows of a company. However, it is generally recommended to revise Cash flow planning on a weekly basis. For liability reasons alone.

In this context, there is a very interesting and short article on the topic by the well-known US venture investor Fred Wilson: Cash Management (in Startups). I put the startup in brackets because Fred Wilson's definition of startups is very broad.

Why is Cash flow planning so important?

Ensuring that sufficient Cash position liquidity is available is an intrinsic task of an entrepreneur that should not be delegated. It is the owner's task to appoint a person to ensure Cash position, i.e. to forecast the development of liquidity - or to take on this responsibility themselves. The authority to monitor Cash position can be delegated, but the responsibility for its continued existence remains with the owner.

But why is this the case? Because without Cash position, i.e. without liquid assets (bank balances, cash in hand or utilizable credit lines), companies fail. In legal terms, this means insolvency. Insolvency refers to the situation of a debtor not being able to meet its payment obligations to creditors. Insolvency regulations are in place to minimize the consequences of insolvency.

Misconduct in the sense of insolvency law or even negligence in the monitoring of Cash position can even have consequences under criminal law.

How do you make a Cash flow planning?

The following procedures are possible when creating Cash flow planning :

- Zero base - you start by submitting an empty Cash flow plan and enter the future payment flows, i.e. the expected income or expenses

- Updating the actual figures - the actual figures (account balance + past transactions) are transferred to Cash flow plan and a linear relationship with the development of the past is assumed

- Transfer of figures from the financial plan - the figures from the financial plan are transferred to Cash flow plan

Procedure 2 and 3 are used in practice in combination.

From the financial plan to the Cash flow plan

When transferring the figures from the financial plan to Cash flow plan , the following points should be noted:

- Financial planning takes into account revenues and expenses and NOT outgoing or incoming payments - take into account the average payment terms of your customers or your payment behaviour for supplier invoices, i.e. how long it takes until a transaction is made on the account - in this context, one often speaks of the cash conversion cycle.

- Financial planning is net - while Cash flow planning uses gross values, as the actual cash flows on the accounts are to be forecast

- "Non-cash" items are not included in Cash flow planning - this mainly relates to depreciation and amortization

- If only a planned P&L has been prepared within the framework of financial planning, the planning horizon must be checked for investments as well as divestments.

- The same applies to financing, pay particular attention to loan repayment dates!

- Financing - Note for advanced or managing directors (who are not shareholders): Be aware of dividend payout dates. Even a dividend decided by the shareholders may NOT be paid out in case of imminent insolvency, not even on written instruction. In extreme cases, the managing director may be personally liable.

- Different consideration of the periods in the financial plan and in the Cash flow planning. A financial plan for the following period is usually prepared at the end of a financial year. However, the Cash flow plan always looks at least 6-12 months into the future. This means that no budget figures from the financial plan may be available in the second half of the year.

- Top item: Financial planning does not require a "top item", whereas Cash flow planning is calculated from a current liquidity position (e.g. bank balances). This is because the result of financial planning is a period variable (profit for a period) and the result of Cash flow planning is a point in time variable (Cash position on day X).

What do you need for Cash flow planning?

As shown, Cash flow planning is not only the most important planning but also the easiest to create. You need the following information to create the cash flow statement:

- The current Cash position. This is usually the sum of the account balances of the bank accounts (bank credit balances), but also the cash balances. Attention, do not forget e.g. Paypal credit balances here.

- Assumptions about future cash flows that will change the current level of cash and cash equivalents.

- Indicators for the assumptions in the short-term area are the open items

- A financial plan or the historical actual figures from previous periods can help to guide the assumptions in the medium term.

- The assumptions in the long-term area are based on the entrepreneurial objectives or priorities. For example, if one wants to achieve a growth in turnover, allow for higher private withdrawals, etc., one should consider the following

Ongoing maintenance or rolling maintenance Cash flow planning

By using rolling planning, you can continuously monitor the goals you originally set and - based on facts - revise them if necessary. What sounds so simple now is in practice tedious to create but above all to maintain and keep up to date.

In our view, there are two points to bear in mind. The Cash flow planning must always be kept up to date and no budgets should be "forgotten". Up-to-date planning can be achieved by assigning an employee to regularly monitor the bank accounts and consolidate them in a planning tool of some kind. This could be in Excel or in your ERP.

While another approach chosen is also "I have a feeling about this", this approach is STRONGLY not recommended. The most important point, however, is that if something does happen, as a managing director you will quickly find yourself in a situation of "gross negligence" and thus in an insolvency delay (= criminal law).

And what is this about forgetting budgets?

Let's assume that you have planned a turnover of 10,000 in one month, but only 8,000 come in. The responsible employee assures you that the 2,000 will be "made up" at a later date. In a simple target/actual comparison, this information is a comment. In the case of rolling planning, the future budget must be adjusted by the 2,000 to be made up. This applies not only to incoming payments, but especially to outgoing payments. As Cash flow planning should always be kept conservative, see also the topic of provisions in Cash flow planning, positive deviations in payments should be carried forward to the following months in case of doubt. In other words, it is assumed that these costs "saved" in the months will still be incurred at a later date. Ideally, these costs will not be incurred after all and you will have built up a liquidity reserve or "provision". And nothing is more pleasant than having a small buffer!

Special topics in the Cash flow planning

Value added tax in the Cash flow planning

The aim of Cash flow planning is to map future cash flows, i.e. incoming and outgoing payments. In principle, these payments are always made gross. As a rule, the service provider owes the sales tax to the tax office. VAT is an annual tax with monthly or quarterly VAT prepayments. This means that these advance payments must be planned in a cash-effective manner. Since the entrepreneur making the payment owes the tax, the entrepreneur receiving the service may deduct the VAT paid by him (input tax) when calculating the VAT prepayments. The VAT rates applicable in each EU country must be used for the calculations.

Ever wondered why some invoices say 0% VAT reverse charge?

An exception is the so-called reverse charge procedure within the EU. This leads to a reversal of the tax liability in defined cases. Haufe has presented the benefits very clearly: Reverse charge

The reverse charge procedure mainly applies to deliveries and services within the EU and depends on the place where the service is provided. De facto, this leads, for example, in the case of digital services such as Google Ads, COMMITLY, etc., to a display of 0% VAT and the corresponding reference: "Subject to the reverse charge procedure".

The correct mapping of VAT can therefore take all forms, from simple to very complex. Since complexity is the enemy of simplicity and Cash flow planning should be kept as simple as possible, a pragmatic approach has emerged in practice.

It is assumed that all inputs and outputs are gross values and the advance VAT payment is taken into account for planning purposes on the basis of the past. Rough changes or fluctuations in the development of turnover and costs are estimated in the forecast.

There is a basic principle in planning: since the future is unpredictable, always plan more conservatively, i.e. with higher costs. Perfect transition to the topic of provisions in Cash flow planning.

Provisions in the Cash flow planning

In accounting, provisions are liabilities whose existence or amount is uncertain, but which are expected with a sufficiently high degree of probability. Explicit provisions in the accounting sense do not exist at Cash flow planning . However, provisions can be formed implicitly in the following ways:

- Plan conservatively - i.e. set income rather low while expected expenditure rather high

- Since the development of the account balance within a month is also important in Cash flow planning , income whose payment date is uncertain should be planned at the end of the month and expenses at the beginning of the month.

- As part of the rolling Cash flow planning , positive deviations in a previous period can be carried over to future periods as a buffer.

Depreciation in the Cash flow planning

In accounting, depreciation is the recognition and offsetting of reductions in the value of fixed and current assets. Reductions in value that occur due to use over time are also referred to as depreciation. These are non-cash expenses (or income) that are not taken into account in Cash flow planning .

Offsetting between several accounts or companies

A special case in financing is transfers between accounts or offsetting between companies. We are often asked how to deal with this issue when using COMMITLY. Technically, these are financings between two companies, we recommend creating a category "Offsets" in the Cash Flow from Financings section. If one wants to be precise, categories could also be created for each account or company and the transactions categorised accordingly.

Cash flow planning and cost centers

We at COMMITLY are familiar with the topic of cost centers from feedback from our users. For this reason, I would also like to address this topic here. For us, this is the difference between a financial and a Cash flow planning and their different objectives.

- Cost centres are indispensable for the control of a company above a certain size

- If you have cost centres, financial planning should also be done at this level.

- The clean mapping of cost centres requires a lot of effort in accounting (account assignment, posting, etc.).

- The primary goal of a cost centre structure in financial planning is the transparent presentation of the financial management of the cost centres, but this is primarily oriented towards the past.

- Cash flow planning is forward-looking and is intended to ensure the company's solvency at all times and to identify financial requirements for action (positive and negative) at company level

In our opinion, Cash flow planning with a cost center structure would be completely excessive and would involve too much effort. In larger companies, these areas are therefore always separated.

Cash flow planning for 13 weeks?

13 weeks is considered an important period in the context of the solvency check. Keyword here is also: the forest stock forecast. If there is an insolvency, the manager must check in the 21-day plan whether the solvency can be restored in this period with a probability bordering on certainty.

https://insoguide.de/zahlungsunfaehigkeit

However, a 21-day plan does not provide sufficient information about the further development of the company's liquidity. A rolling, detailed Cash flow planning over 13 weeks has proven to be more useful. This time period is generally easy to plan due to open items. The topic of forest inventory forecasting is defined in IDW S 11. IDW stands for Institute of Public Auditors in Germany:

"With IDW S 11, the IDW publishes a standard for the assessment of insolvency, over-indebtedness and impending insolvency. Taking into account the current supreme court rulings, it also addresses controversial questions in the literature. Overall, the IDW takes a rather conservative view: According to IDW S 11, a company is insolvent if it cannot completely close even a minor liquidity gap of a few percent of the obligations due on the reporting date in the long term."

IDW: New standard for assessing insolvency maturity

How do you start with a Cash flow planning in COMMITLY?

We were told about the following specific situation during an onboarding session:

- We use an Excel list in which all orders are recorded. (Expected Open Items or also OPOS)

- Details are: Number, supplier, gross amount, expected payment date

- 1x per week on Mondays we receive an OPOS list from the accounting department

- The list is copied to the expected OPOS list.

- The expected OPOS list is compared with the "actual" OPOS and the expected OPOS entry is manually deleted so that only the "actual" OPOS entry is available.

- Originally, the deletion was done manually, but our Excel expert then developed a macro for us to do this

- We have the same procedure for outgoing invoices

- The account balance is updated 1x per month and then everything is adjusted accordingly

- We could automate the process even further in Excel, but we do not want to build up complexity here and depend on our Excel specialists.

Against this background, a start in COMMITLY would make sense as follows: Basic Setup

- Establishment of the company, name + end of business year (Attention, please enter correctly, cannot be changed later)

- Linking the bank accounts

- If necessary, adapt the categories to the requirements of the company - Help area COMMITLY - Create categories

- Categorisation of transactions - please refer to the professional tips in the help section.

- Tip: Please note the threefold division of the cash flow calculation into operating cash flow, cash flow from investment and financing.

Result after the basic setup

- All actual figures sent by the bank are categorised. On the planning screen you can see the cash flow planning (dropdown: actual figures). The chart shows the development to the day.

- Furthermore, you can have a first report created under Reports - Help area COMMITLY - Create Reports

On this basis, you can transfer your OPOS procedure into COMMITLY

- In general, our understanding of OPOS includes "expected OPOS" - Help COMMITLY - What are open items?

- Import of expected OPOS: please note here that expected inputs are positive amounts, outputs are negative amounts. The column headings are to be chosen as mentioned in the help article. The Excel list must not contain any blank lines or formulas. Please also use only 1 spreadsheet. - Help area COMMITLY - Add open items

- After the import, you can also assign the individual entries to categories

- I would do the matching with the "actual" OPOS manually by changing the status of the entry. To change the entries, please see this post: COMMITLY Help Area - Edit Open Items

- I also have a 7 minute video on our Youtube channel on how to do these steps: Demo Open Items

Result after transfer OPOS

- In the OPOS summary, you can see the amount of receivables and payables as well as the time of occurrence graphically.

- On the planning screen, if you select "Forecast" in the drop-down menu (standard selection), you will see the development of the cash flow over the next few months (table), with day-by-day precision in the graph.

Next steps

- Complete the cash flow table Forecast on the planning screen with inputs and outputs that are not transferred via the OPOS (e.g. rent, insurance, accounting, tax advice, etc.) - Tip: Planning is easy by clicking on the desired cell (category and month) and planning an amount - basic procedure here: Help area COMMITLY - Create planning

- Synchronise - by clicking on the synchronisation button, the bank account will be updated. New transactions (if any) are loaded and the account balance is updated. The new transactions must be categorised. In the background, your new assistant Wolff learns and already makes the first suggestions. This will get better and better over time.