Cashflow oder Cashflow Planung waren noch nie so wichtig für Unternehmen wie heute. In diesem Artikel erfahren Sie alles über die Cash Flow-Berechnung in Unternehmen – einfach erklärt und sofort nachvollziehbar.

Man muss kein BWL-Absolvent oder ausgebildeter Steuerberater sein, um eine Cashflow-Berechnung vornehmen zu können. Im Gegenteil: Die Cashflow Berechnung ist das einfachste Kennzahlensystem, das in einem Unternehmen intern eingesetzt werden kann. Vor allem, wenn man die direkte Methode heranzieht. Aber dazu kommen wir noch!

Unabhängig davon, ob man die Liquiditätssituation, Finanzkraft oder das Potential für Gewinnausschüttungen prognostizieren möchte – mithilfe der Kennzahlen des Kapitalflusses haben Unternehmer, Betriebswirte, Banken sowie Investoren einen schnellen Einblick in den Gesundheitszustand eines Unternehmens.

Was ist der Cashflow (Cash Flow)?

Cashflow was ist das? Der Cashflow (auch Cash Flows, englisch für Geldfluss, Zahlungsfluss, Einzahlungen Auszahlungen) ist eine wichtige Kennzahl über die Finanzkraft von Unternehmen (Kennzahl Cashflow). Der Cash Flow gibt dabei Auskunft über die Liquiditätssituation und über den Geldfluss (Einzahlungen Auszahlungen), der in einer bestimmten Abrechnungsperiode stattgefunden hat oder stattfinden wird.

In einer engeren Definition bezeichnet Cashflow lediglich den Zufluss bzw. Abfluss liquider Mittel aus der sogenannten gewöhnlichen Tätigkeit eines Unternehmens (Betrieblicher Cashflow). Unbare Ein- und Ausgaben bzw. nicht zahlungswirksame Vorgänge (z. B. Abschreibungen und Rückstellungen) werden im Cashflow nicht berücksichtigt. In der weiteren Definition werden dem Cashflow auch Zu- und Abgänge an Geld aus den Bereichen der Investitionen und der Finanzierung zugeordnet.

Fazit: Liquidität ist also eine Zeitpunktbetrachtung. Der Cashflow als Kapitalflussrechnung ist eine Betrachtung der Veränderung der Liquidität über einen Zeitraum. Dadurch sieht man, wie viel Geld während einer definierten Zeitperiode (üblicherweise Monat, Quartal, Jahr) einem Unternehmen zu bzw. abfließt – deshalb auch die Bezeichnung Geld- oder Zahlungsfluss.

Verlust trotz positivem Cashflow-Ergebnis?

Cashflow was sagt er aus? Bestimmt kennen Sie die folgende oder eine ähnliche Aussage: „Das Unternehmen hat einen positiven Cashflow, hier sollte man investieren!“

Macht auf den ersten Blick auch Sinn. Mehr Zuflüsse als Abflüsse bedeutet doch mehr Gewinn, oder?

Aus Sicht eines Steuerberaters oder Buchhalter ist dies jedoch nicht korrekt, da verschiedene Systeme miteinander vermischt werden. Gewinn wird durch eine GuV auf Basis der Buchhaltung ermittelt, Zu- und Abflüsse sind Begriffe der Cashflow Berechnung (Cashflow Plan).

Warum die Formel nicht automatisch zu einem Gewinn führen muss bzw. warum der Gewinn auch wesentlich geringer sein kann, sieht man bei einer genaueren Betrachtung der Ermittlungsmethoden.

Was ist der Unterschied zwischen der direkten und der indirekten Cashflow-Berechnung?

Wie Cashflow berechnen? Grundsätzlich gibt es bei der Cashflow-Berechnung zwei Berechnungsmethoden: die „direkte Berechnung“ und die „indirekte Berechnung“.

Beide Cashflow- oder auch Kapitalflussrechnungen sind gängig und führen zum selben Ergebnis. Wann man welche Methode anwendet, ist jedoch bedarfsabhängig und abhängig von den verfügbaren Informationen.

Liegen keine internen Informationen über Eingänge und Ausgänge vor bzw. ist man auf öffentliche Quellen angewiesen, wir die indirekte Methode angewendet. Die indirekte Methode wird daher hauptsächlich eingesetzt, um auf Basis eines vorhandenen Jahresabschlusses (Bilanz und GuV) die Liquiditätssituation zu beurteilen.

Die direkte Methode kann aufgrund ihrer Einfachheit im Unternehmen selbst jederzeit intern als Kennzahlensystem eingesetzt werden.

Sehen wir uns die beiden Berechnungsmodelle im Vergleich an.

Direkte Cashflow-Berechnung vs. Indirekte Cashflow-Berechnung

Direkte Cashflow-Berechnung

Vorteilhaft bei der direkten Berechnung Cash Flow ist die Einfachheit und somit Geschwindigkeit dieser Variante, mit der Sie zu einem Ergebnis kommen. Als Nachteil wird bei dieser Berechnungsmethode oftmals die mangelnde Überprüfbarkeit bemängelt, da in der Regel interne und ungeprüfte Informationen dafür herangezogen werden.

Nochmals erwähnt: der Cashflow bzw. der Kapitalfluss ist eine zeitlich eingeschränkte Momentaufnahme des Geldflusses, der Zahlungsströme. Das heißt: Welches Ergebnis habe ich in der selbst definierten Periode (beispielsweise ein Monat), wenn ich die Ausgänge von den Eingängen subtrahiere?

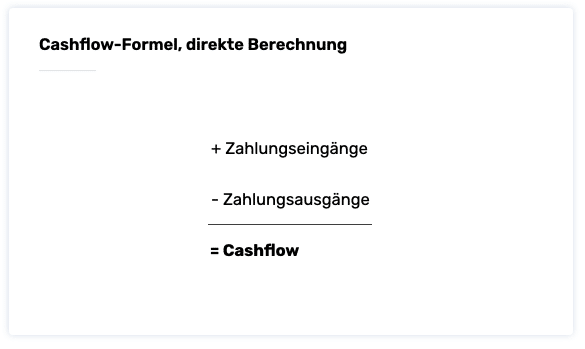

Cashflow-Formel der direkten Berechnung:

Zahlungseingänge minus Zahlungsausgänge = Cashflow

Als Eingänge werden alle zahlungswirksamen Erträge verbucht. Beispielsweise:

- Einzahlungen aus Umsätzen / Forderungen

- Sonstige Einzahlungen wie etwa Eigenkapitaleinlagen

- Kreditaufnahme

- Etc.

Als Ausgänge werden alle zahlungswirksamen Aufwendungen verbucht. Beispielsweise:

- Auszahlungen für Personal und Verbindlichkeiten

- Auszahlungen für Material und Waren

- Sonstige Auszahlungen

- Kredittilgung

- Etc.

Direkter Cashflow einer Privatperson – (Beispiel Student)

Wenn ich als Student 300 Euro Miete, 300 Euro für Lebensmittel und 400 Euro für andere Interessen ausgebe, aber nur 800 Euro im Nebenjob verdiene, ist der Cashflow um 200 Euro negativ.

Die konkrete Kapitalflussrechnung lautet:

(EINGÄNGE: 800 – AUSGÄNGE: 1.000) = -200 Euro Cashflow.

Direkter Cashflow eines Unternehmens – (Beispiel Agentur)

Im Fall einer Büro-Nettomiete von 4.000 Euro, Lohnkosten von 12.000 Euro, 7.500 Euro Werbekosten iegt man bei 23.500 Euro auf der Ausgaben Seite. Die Einnahmen durch die Agentur-Dienstleistung ergeben sich netto 35.000 Euro. Der Cashflow ist somit mit 11.500 Euro positiv.

Die konkrete Kapitalflussrechnung lautet:

(EINGÄNGE: 35.000 – AUSGÄNGE: 23.500) = 11.500 Euro Cashflow.

Indirekte Cashflow-Berechnung

Diese Berechnungsmethodik ist unter Steuer- und Unternehmensberatern oder erfahrenen Betriebswirten die bevorzugte bzw. einzig mögliche, da die Voraussetzung dafür ein ordentlich aufgestellter Abschluß, in der Regel ein Jahresabschluß, ist und dieser verfügbar ist. Als Nachteil wird hier oftmals die Komplexität der erforderlichen Datenerhebung genannt.

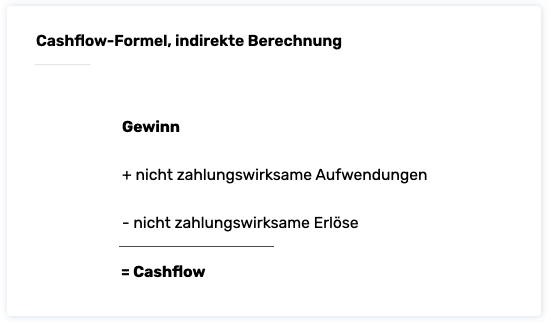

Cashflow-Formel der indirekten Berechnung:

GEWINN plus nicht zahlungswirksame Aufwendungen minus nicht zahlungswirksame Erlöse = Cashflow

Die indirekte Berechnung ist in der Kalkulation komplex und aufgrund erforderlicher Daten meist nur bedingt eigenständig möglich. Vor allem ist für die Berechnung eine abgeschlossene (Buchhaltungs)Periode erforderlich, meistens ein abgeschlossenes Geschäftsjahr. Mit Unterstützung eines Steuerberaters oder Buchhalter ist die indirekte Cashflow-Berechnung jedoch ebenfalls eigenständig kalkulierbar. Auch hier gilt eine definierte Periode – im Fall der indirekten Berechnung meistens ein Geschäftsjahr.

Unter nicht zahlungswirksamen Aufwendungen (unbare Aufwendungen) versteht man:

- Abschreibungen

- Bildung von Rückstellungen

- Rechnungsabgrenzungen

- Abschreibung Forderungsverluste

- Etc.

Unter nicht zahlungswirksamen Erträgen (unbare Erlöse) versteht man:

- Auflösung von Rückstellungen

- Bewertungsgewinne (bei Immobilien)

- Bestandserhöhungen

- Aktivierte Eigenleistungen

- Etc.

Konkret: Gewinn plus nicht zahlungswirksame Aufwendungen – oft auch als unbare Aufwendungen bezeichnet – (Abschreibungen Forderungen sowie Rücklagen) minus nicht zahlungswirksame (unbare) Erlöse (Zuschreibungen aufgrund z.B. von höheren Bewertungen) = Cashflow.

Indirekter Cashflow eines Unternehmens – (Beispiel Handwerksbetrieb)

Ein Handwerksbetrieb erwirtschaftet einen Gewinn von 60.000 Euro in diesem Geschäftsjahr. Die Rückstellungen und Abschreibungen liegen lt. Jahresabschluß in diesem Jahr bei 20.000 Euro. Zusätzlich wurden im Abschluß Prozesskostenrückstellungen in Höhe von 15.000 Euro ausgewiesen. Die Druckerei hat somit nach der indirekten Cashflow-Berechnung einen Cashflow von 95.000 Euro erwirtschaftet.

Die indirekte Kapitalflussrechnung lautet:

(GEWINN: 60.000 + n.z.w. AUFWENDUNGEN: 35.000) = 95.000 Euro Cashflow.

Fazit zur direkten und indirekten Cashflow-Berechnung

Anhand der oben angeführten Beispiele kann man erkennen, dass die Variablen Gewinn, Rückstellung und Abschreibung durchaus dazu führen können, dass sich das Ergebnis dahingehend verändert, dass das Geschäftsjahr zwar positiv ist, die tatsächlich erwirtschaftete Liquidität wesentlich höher sein kann. Das Problem ist, dass auch genau das Gegenteil der Fall sein kann.

Mit Hilfe der Cashflow-Berechnung können damit Spielräume bei der Erstellung von Jahresabschlüssen (gerne auch als Bilanztricks bezeichnet) offengelegt und die tatsächliche Liquiditätssituation des Unternehmens dargestellt werden.

Die Cashflow-Formeln (zur Erinnerung)

Mit den beiden Cashflow-Formeln gelingt Ihnen jede Berechnung der Zahlungsströme ganz einfach. Die Formel der direkten Cashflow-Berechnung liefert rasche Einblicke in die finanzielle Situation, die Formel der indirekten Cashflow-Berechnung hingegen ist detaillierter und bietet daher einen genaueren Einblick in die Liquidität eines Unternehmens.

- Cashflow-Formel der direkten Berechnung:

EINGÄNGE minus AUSGÄNGE = Cashflow - Cashflow-Formel der indirekten Berechnung:

GEWINN plus nicht zahlungswirksame Aufwendungen minus nicht zahlungswirksame Erlöse = Cashflow

Welche Bedeutung hat der Cashflow in Bezug auf die Liquidität?

Durch das Ergebnis der Kapitalflussrechnung, dem aktuellen Cashflow, lassen sich Rückschlüsse auf die Liquidität ziehen:

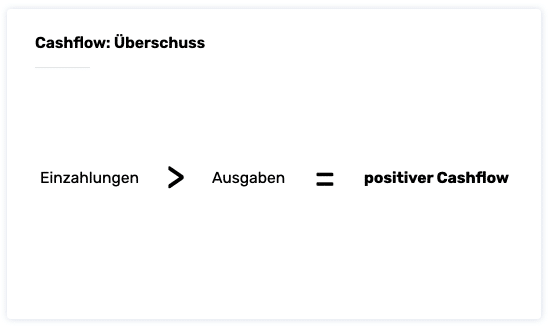

Positiver Cashflow = Liquidität (Überschuss)

Fällt der Cashflow positiv aus, bedeutet dies, dass ein Überschuss in der betrachteten Periode, z.B. einem Monat, besteht.

Ausgaben < Einnahmen = positiver Cashflow = Überschuss

Ist der Cashflow positiv, sind also die Ausgänge niedriger als die Eingänge in der betreffenden Periode und es entsteht ein Überschuss. Die Liquidität ist somit gegeben und es können Zahlungen getätigt, Schulden getilgt oder Investitionen getätigt werden.

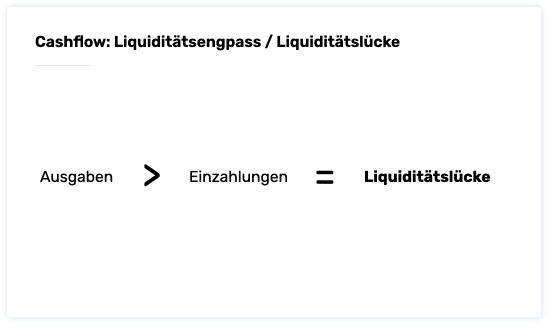

Negativer Cashflow = Liquiditätsengpass oder Liquiditätslücke

Fällt der Cashflow negativ in einer Periode aus, bedeutet dies, dass eine Liquiditätslücke in dieser Periode besteht.

Ausgaben > Einnahmen = negativer Cashflow = Liquiditätslücke

Ist der Cashflow negativ, sind also die Ausgaben höher als die Einnahmen in einer Periode entsteht ein Liquiditätslücke. Bestanden am Anfang der Betrachtung keine Cash Bestände ist die Liquidität somit nicht gegeben und es können vorübergehend – also für den Zeitraum des Liquiditätsengpasses – keine Zahlungen getätigt, keine Schulden getilgt und keine Investitionen getätigt werden. In diesem Fall stellt sich die Frage, ob zum Beispiel anderweitig verfügbare Mittel, wie z.B. nicht ausgenutzte Kontokorrentlinien zur Verfügung stehen.

Das Schema der direkten Cashflow Ermittlung im Detail

COMMITLY setzt als Rahmen (Template) für die Liquiditätsplanung die sogenannte direkte Cash Flow Ermittlung ein. Im Finanzjargon bedeutet das, dass zahlungswirksame Erträge mit den zahlungswirksamen Aufwendungen saldiert werden. Auf gut Deutsch heißt das, dass wir den verfügbaren Cash Flow oder auch Free Cash Flow als Differenz zwischen den Zahlungseingängen und den -ausgängen auf allen (verbundenen) Konten errechnen.

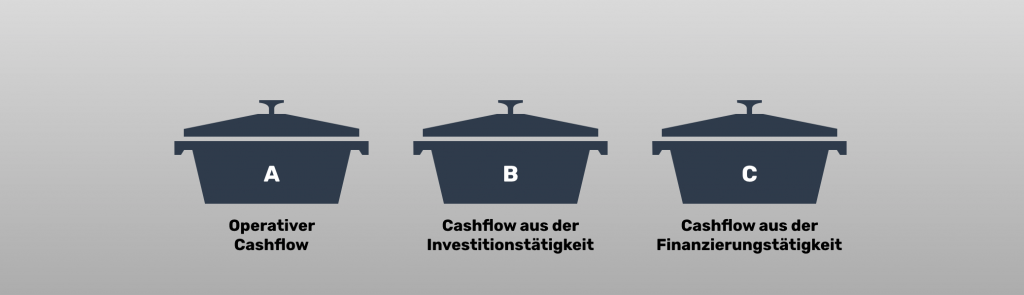

Bei der Berechnung werden die Ein- und Ausgänge in 3 Gruppen unterteilt:

A – Der Operative Cashflow (Operating Cashflow)

Der operative Cashflow (operating cashflow) gibt an, ob dein Unternehmen in der Lage ist, sich selbst zu finanzieren. Wenn die laufenden Einnahmen (Zahlungseingänge) in einem bestimmten Zeitraum höher sind als deine laufenden Ausgaben (Zahlungsausgänge), ist alles im grünen Bereich. Weiter so! Ein langfristig positiver operativer Cashflow (operating cashflow) ist für den Fortbestand von wesentlicher Bedeutung.

B – Cash Flow aus der Investitionstätigkeit

Dieser Topf gibt an, ob du für dein Unternehmen Investitionen getätigt hast oder Vermögensgegenstände gekauft hast. Wenn dein Cash Flow aus der laufenden Geschäftstätigkeit positiv ist, d.h. Geld vorhanden ist bzw. übrig bleibt, hast du die Möglichkeit, Investitionen zu tätigen, also z.B. einen neuen Arbeitsplatz inkl. PC zu kaufen.

C – Cash Flow aus der Finanzierungstätigkeit (Cashflow Finanzierungstätigkeit)

Dieser gibt an, ob dein Unternehmen Kredite aufgenommen oder getilgt hat oder Auszahlungen an die Gesellschafter vorgenommen hat (Dividenden) bzw. Einzahlungen von Gesellschafter erhalten hat. Eine Entnahme über den Unternehmerlohn hinaus fällt auch in diese Kategorie. Wenn die operative Geschäftstätigkeit zu wenig Cash Flow liefert, kannst du auch aus diesem Topf, z.B. mit deinem Unternehmenskredit, Investitionen tätigen. (Cashflow Finanzierungstätigkeit)

Cashflow optimieren – warum sind diese drei Bereiche aber eigentlich so wichtig?

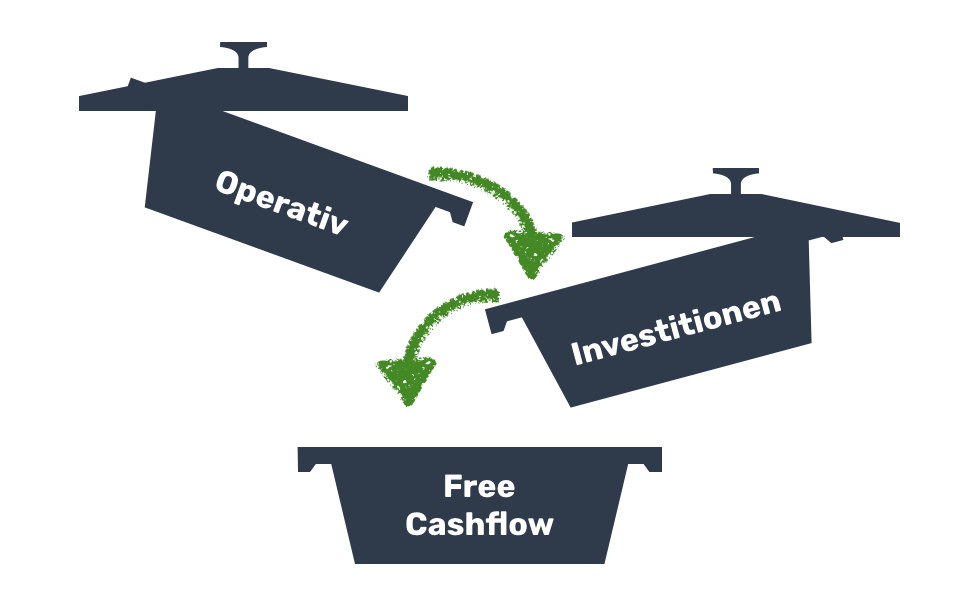

Weil sie zusammen die Finanzkraft deines Unternehmens bestens abbilden. Damit sind auch alle Hebel transpartent, um den Cashflow optimieren zu können. Wir haben in unserem Beispiel den Best Case dargestellt: Deine Geschäfte laufen so gut, dass du aus deinen laufenden Einnahmen einen Überschuss erzielst, investieren kannst und dir sogar noch etwas überbleibt. Das was übrig bleibt ist dann übrigens der „Free Cash Flow“.

Ein positiver frei verfügbarer Cashflow / Free Cash Flow

Der positive „free cashflow“ (Freie Cashflow) steht dir, wie der Name schon sagt, zur freien Verfügung. Das heißt, du hast alle laufenden Ausgaben gedeckt, hast Investitionen getätigt und es ist noch etwas übergeblieben. Gratulation!

Was tut man am besten mit dem Free Cashflow (Freie Cashflow)?

- Einen Liquiditätspuffer als Vorsorge aufbauen

- In neue Projekte oder etwa neue Mitarbeiter investieren

- Kredite vorzeitig zurückzahlen

- Gewinne entnehmen

- …

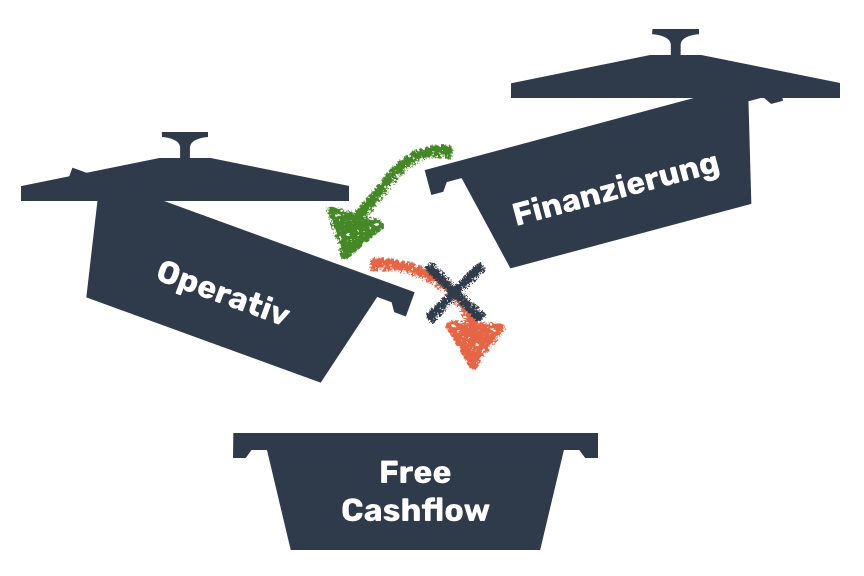

Was tun bei einem negativen operativen Cashflow / negativen Free Cashflow?

Doch was ist, wenn dein operativer Cashflow negativ ist (negativer operativer Cashflow), das heißt, wenn deine Ausgaben (Zahlungsausgänge) höher sind als die Einnahmen (Zahlungseingänge)?

Erstens: Nicht verzweifeln! Zweitens: Halte dir vor Augen, dass du nicht alleine mit diesem Problem bist! Beinahe jeder Unternehmer kennt diese Situation: In einem Monat haben sich die Zahlungseingänge verspätet und nicht alle Ausgaben können reibungslos gezahlt werden.

Glücklich, wer sich aus der Vorperioden einen Liquiditätspuffer aufgebaut hat. Dann handelt es sich nur um einen temporären Liquiditätsengpaß. Wenn nicht, hilft nur der Cashflow aus Finanzierung – also der Griff in die eigenen Taschen oder der Gang zum Investor oder der Bank.

Cashflow optimieren / Cashflow steuern – welche Maßnahmen können also getroffen werden?

- Cashflow Plan erstellen!

- Prüfen, ob Investitionen nach hinten geschoben werden können und welche Auswirkungen das auf den Cashflow Plan hat

- Wenn es verwertbares Anlagevermögen gibt, kann evtl. auch eine Veräußerung (Devestition) geprüft werden.

- Finanzierung – gibt es Zugriff auf Darlehen, Förderungen, frisches Eigenkapital

- Ebenfalls in den Bereich der Finanzieurng fällt der Verzicht auf Entnahmen

- Alle Maßnahmen im Cashflow Plan abbilden, damit werden auch Gespräche mit potentiellen Finanzierungspartnern wesentlich einfacher

Stellt die Cashflow Planung damit ausschließlich auf die Bankkonten ab?

Die kurze Antwort ist: Ja!

Aber was ist mit den Daten aus der Buchhaltung? Hauptaufgabe der Buchhaltung ist die gesetzlich korrekte Abbildung der Vergangenheit. Die Planung betrifft die Zukunft, hat keine gesetzlichen Vorgaben UND man kann auch nichts „kaputt“ machen. Das ist ein wichtiger Aspekt, der auch von unseren Kunden angeführt wird. Der bekannte Investor Fred Wilson hat in seinem Blog auch einen anderen sehr wichtigen Aspekt beschrieben – unterschiedliche Typen. Die Finanzfunktion: Rückblick und Blick nach vorne

„Meiner Erfahrung nach sind die Menschen, die in der Rückschau-Funktion stark sind, oft nicht in der Vorwärts-Funktion stark. Möglicherweise benötigen Sie verschiedene Personen, um diese Rollen zu übernehmen. In einem großen Unternehmen gibt es ganz unterschiedliche Abteilungen, die diese Funktionen übernehmen. Es gibt eine Buchhaltungsabteilung und eine Finanzplanungsabteilung (oft FP&A genannt).“

Ist die direkte Cashflow Planung damit nur für Einahmen Überschuss Rechner sinnvoll?

Nein! Unternehmen mit doppelter Buchführung haben aus der Buchhaltung heraus gerade limitierten Einblick in ihren Cash Flow. Das führt dann oft dazu, dass die indirekte Methode zur Ermittlung des Cash Flows herangezogen wird. Aufsatzpunkt dabei ist dann das Periodenergebnis und es werden sogenannte non-cash items, also nicht zahlungswirksame Erlöse und Aufwände wie z.B. Abschreibungen herausgerechnet. Zusätzlich hat man noch Themen mit Periodenabgrenzungen. Die indirekte Ableitung ist aber so kompliziert, dass das in der Regel vom Steuerberater gemacht wird, mit entsprechender zeitlicher Verzögerung.

Ist die indirekte Ermittlung nicht doch besser für größere Unternehmen?

Der direkt ermittelte Cashflow Plan, wie von COMMITLY eingesetzt, ist super einfach und deckt alle Szenarien und auch Buchhaltungsformen UND auch Unternehmensgrößen ab. Das „Verbindungsstück“ wenn man so will, ist der Cashbestand bzw. der Kontostand der Banken. In der Praxis haben wir selten (eigentlich nie) Liquiditätsplanungen (und auch Cash Flow Berichte) in Excel gesehen, die 1:1 mit der Buchhaltung abstimmbar waren. Ein Tool wie COMMITLY gewährleistet die Abstimmbarkeit.

Warum? Weil am Ende einer Periode die wichtigste Basis eines Steuerberaters (egal ob EÜR oder doppelte Buchhaltung) die Abstimmung mit dem Bankkonto ist. Und das ist automatisch in COMMITLY gewährleistet.

Credits: Foto von pixabay, by Stevepb