Viele Gründer stehen ganz am Anfang ihrer Karriere. Sicherlich gibt es bereits erfolgreiche Gründer, die über das notwendige Kapital verfügen, die Mehrheit muss allerdings nach Wegen suchen, wie sie ihre Gründung und die erste Zeit finanzieren kann. Oft ist es daher nicht einfach, einen Kredit zu bekommen. Selbständige gehören selten zu den Lieblingskunden einer Bank. Aber wie gelingt der Erhalt eines Unternehmerkredits in der Gründungsphase?

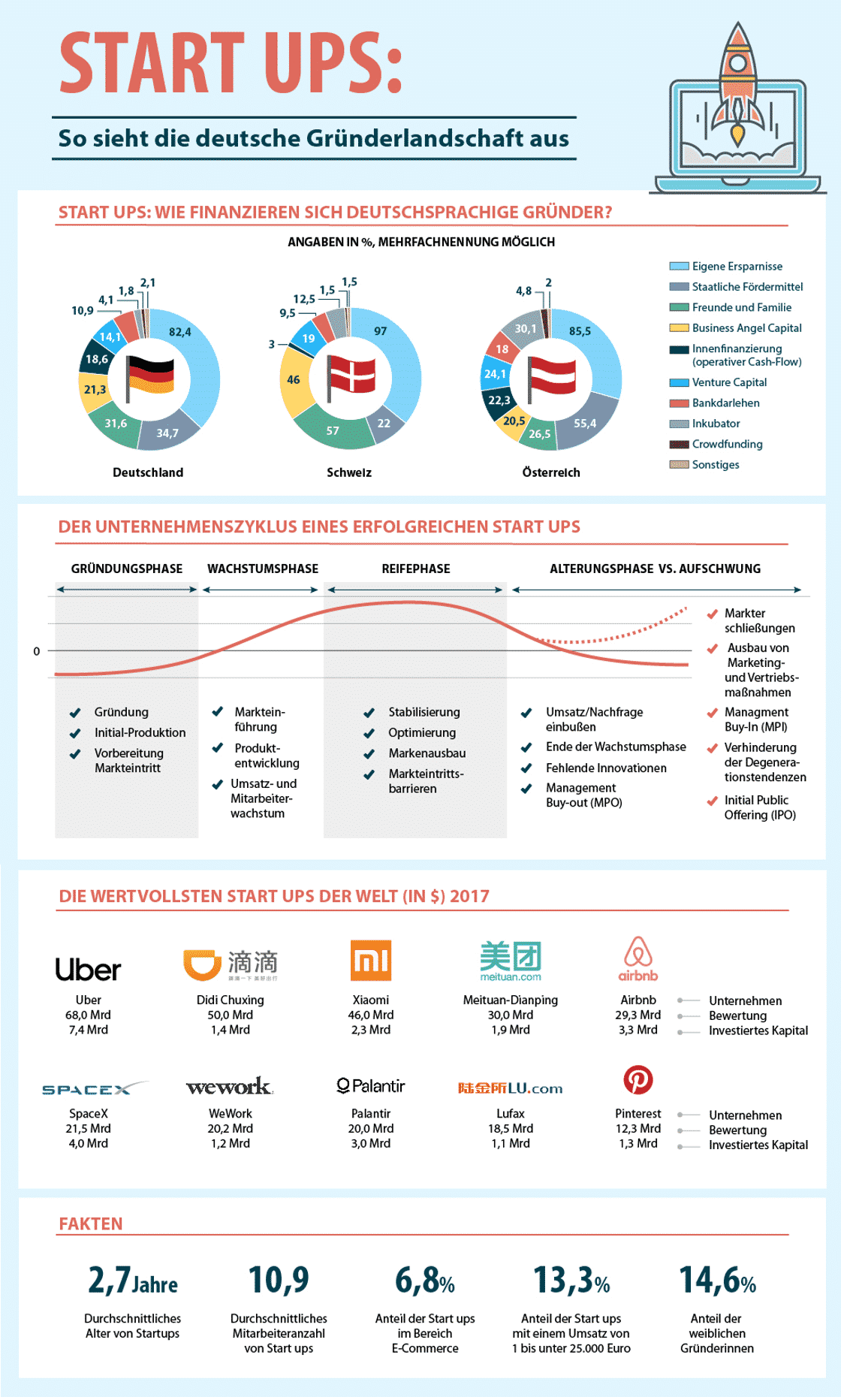

Abbildung 1: Start-Ups in Deutschland bauen auf verschiedene Finanzierungsquellen. Oft stehen dabei Eigenmittel im Fokus. Doch was, wenn eine zusätzliche Finanzspritze nötig wird? Bildquelle: @ Smava.de

Die Situation von Gründern im Überblick

Viele Gründer befinden sich in der Lage, noch über kein ausreichendes finanzielles Polster zu verfügen. Es mag zwar Ersparnisse geben, aber diese werden in vielen Fällen bereits in die eigene Geschäftsidee investiert. Unter dem Strich bleibt häufig jedoch wenig bis gar ein Eigenkapital.

Für Banken bedeutet das:

1. Kaum belastbares Einkommen

Das Einkommen des Gründers ist nicht sicher. Ein Unterschied besteht bei Gründern im Nebenerwerb, da diese das Einkommen aus dem Hauptjob vorweisen können. Einkommen aus reiner Selbstständigkeit wird von Banken stets mit einem gewissen Zweifel betrachtet, denn es ist keinesfalls garantiert. Umsätze unterliegen Schwankungen und sind gerade zu Beginn keinesfalls sicher zu kalkulieren. Zudem besteht nur selten und kurzfristig ein Anspruch auf Arbeitslosengeld. Geht die Gründung schief, müssten Gründer auf Hartz 4 zurückgreifen und könnten ihren finanziellen Verpflichtungen nicht mehr nachkommen.

2. Kaum Sicherheiten

Auch sie sind meist rar gesät. Natürlich gibt es Gründer, die bereits ein abbezahltes Eigenheim oder auch hochwertige Kunstobjekte besitzen, das ist aber eher die Seltenheit. Im Normalfall lässt sich für den Unternehmenskredit keinerlei Sicherheit hinterlegen.

Tatsächlich ist es oft schwierig, als Gründer eine Bank zu überzeugen. Aus diesem Grund stehen herkömmliche Unternehmenskredite auch nicht an der Spitze der Finanzierungsmöglichkeiten für Start-Ups.

Vielfach stehen sich die Gründer auch selbst auf den Füßen, denn übertriebene Erwartungen und Berechnungen sind am Ende ein Stolperstein. Doch all das Wissen hilft dem Gründer nicht weiter, denn in seiner Situation benötigt er einen Unternehmerkredit für:

- Aufbau – ob nun Büroflächen, Lagerräume oder auch Produktionshallen oder Labore erstellt oder erweitert werden müssen, ist unerheblich. Das Geld dafür ist notwendig.

- Ausstattung – je nach gegründetem Betrieb variiert diese natürlich. Doch gewisse Anlagen oder Ausstattungen benötigt fast jedes neu gegründete Start-Up.

- Rechtskosten – auch diese sind nicht zu unterschätzen. Ein Gründer ist gut beraten, Fachanwälte an seiner Seite zu haben. Kaum ein Gründer vollbringt es, einen Patentantrag korrekt und umfassend selbst einzureichen.

Hinweis: Wurde schon ein Patent erfolgreich angemeldet, so kann sich das positiv auf die Kreditaufnahme auswirken. Der Grund ist recht simpel: Das erdachte Produkt kann nicht mehr ohne Weiteres von Fremdfirmen auf den Markt gebracht werden – die Absatzchancen und damit die Einnahmen steigen also.

Welche Voraussetzungen müssen Gründer für Bankkredite erfüllen?

Jeder Unternehmensgründer sollte sich perfekt auf den Kreditantrag vorbereiten. Das bedeutet, dass er nicht nur über die möglichen Fördermittel Bescheid weiß, sondern sich und seinen Betrieb im besten Licht präsentieren kann. Aber was gehört dazu?

- Businessplan – die wenigsten Banken können ein gegründetes Unternehmen, dessen Produkte und Chancen einschätzen. Ein hervorragender – und professioneller – Businessplan ist somit die erste Grundlage. Anhand des Plans können die Kreditnehmer die Unternehmenschancen aufzeigen und haargenau erklären, wie sie ein konkretes Ziel erreichen wollen. Wesentlicher Bestandteil des Businessplans ist auch ein daraus abgeleiteter Liquiditätsplan, in dem die Rückführung des Bankkredits abgebildet wird. Ohne den Businessplan besteht höchstens dann die Chance auf einen kleinen Kredit, wenn das Unternehmen im heimischen Wohnzimmer eingerichtet wird und auch sonst kaum Anschubkosten bestehen.

- Bürgen/zweite Kreditnehmer – möglich ist auch die Nutzung eines Bürgen für den Unternehmerkredit. Allerdings muss der Bürge wiederum die Anforderungen der Bank erfüllen und alle Seiten müssen sich darüber im Klaren sein, dass der Bürge, im Fall des Untergangs des Unternehmens, für den Kredit haftet. Dasselbe gilt für einen zweiten Kreditnehmer, dessen Haftung mitunter noch weitergeht.

- Eigenkapital – je mehr Eigenkapital vorhanden ist, desto besser stehen die Chancen auf eine Kreditvergabe. Eigenkapital bedeutet dabei nicht, dass die Gründer das Geld selbst angespart haben müssen. Auch Finanzspritzen aus dem Familien- und Freundeskreis können als Eigenkapital gelten. Dasselbe gilt für Grundstücke, sofern sie unbelastet sind. Grundsätzlich ist es ratsam, bei einem Unternehmenskredit zumindest 10-15% der benötigten Summe als Eigenkapital vorweisen zu können.

Tatsächlich haben oft Gründer bessere Chancen, wenn sie noch einen Angestelltenjob vorweisen können. Dieser dient als Sicherheit gegenüber der Bank. Wichtig ist nur, genau abzuklären, welche Vorstellungen die Bank hinsichtlich des Arbeitsverhältnisses hat. Sicherlich nutzen etliche Gründer ein Angestelltenverhältnis, um die Gründung im Nebenerwerb gut und sicher in die Wege zu leiten, planen aber, an Tag X vollständig im eigenen Unternehmen zu arbeiten. Es wäre denkbar, dass die kreditgebende Bank das Anstellungsverhältnis für eine gewisse Zeit vorschreibt.

Wie können sich Gründer sonst noch Kapital beschaffen?

Viele Gründer stehen vor einem riesigen Dilemma. Sie haben eine grandiose Idee, von deren Erfolg sie wirklich überzeugt sind. Doch um diese Idee im größeren Rahmen umzusetzen, ist Geld nötig – und das erhalten sie nicht, weil sie finanziell keine Sicherheit bieten können. Es hat durchaus seine Gründe, weshalb etliche Existenzgründer durch spezielle TV-Formate tingeln oder anderweitig nach Investoren suchen. Doch wenn herkömmliche Kredite nur schwierig oder gar nicht möglich sind, gilt es, sich nach Alternativen umzuschauen. Grundsätzlich gibt es nämlich durchaus Optionen, um das benötigte Kapital zu erhalten:

- Förderprodukte – auf regionaler Ebene gibt es oft spezielle Fördermittel, die für Start-Ups aus der Region gedacht sind. Je nach Wohnort gibt es ganze Förderkreise, die sich mitunter als nützlich erweisen. Können sie die Mittel nicht bereitstellen, so versuchen sie wenigstens, erfolgversprechende Gründer mit finanzstarken Partnern zusammen zu bringen. Auch auf der EU-Ebene gibt es einige Fördermittel, die zumindest

- KfW-Förderung – über die KfW können Gründer das »Startgeld« und einen weiteren Gründerkredit erhalten. Während der Kapitalkredit für die Gründung dazu gedacht ist, das Eigenkapital eines Unternehmens zu stärken, ist das StartGeld tatsächlich für die Gründung, die laufenden Kosten und Investitionen gedacht. Das StartGeld wird mit bis zu 125.000 Euro ausgegeben, der Kapitalkredit mit bis zu 500.000 Euro. Der Vorteil dieser Förderkredite liegt darin, dass die KfW das vollständige oder zumindest teilweise Kreditrisiko übernimmt und die Tilgungsraten extrem human ansetzt. Darüber hinaus lassen sich je nach Förderprogramm zunächst tilgungsfreie Jahre einplanen, in denen lediglich Zinsen fällig werden. Somit erhält das junge Unternehmen zunächst etwas Zeit, um die Investitionen erfolgreich zu platzieren. Zudem ist es auch möglich, die Kredite in Anspruch zu nehmen, wenn die Gründung schon einige Zeit her ist. Das StartGeld kann bis zu fünf Jahre nach der Unternehmensgründung beantragt werden.

- KfW: KMU-Förderkredit – dieser richtet sich an kleine und mittlere Unternehmen, die auch neu gestartet werden. Auch Freiberufler können den Kredit beantragen. Die Summe liegt im Millionenbereich. Dieser Kredit ist eher für die Gründer von Interesse, die den ersten Schritt schon bewältigt haben und sich nun erweitern wollen.

- Private Darlehen – sie stellen eine gute Möglichkeit dar, sofern sich in der Familie oder im Bekanntenkreis entsprechend finanzkräftige Personen befinden. Bei einem Privatdarlehen ist allerdings stets ein echter Kreditvertrag notwendig, der über die Summe, die Rückzahlungsvereinbarungen, Fristen und Zinsen aufklärt. Leider gilt ihr das Sprichwort, das beim Geld die Freundschaft aufhört und ohne eine schriftliche Form kann jede Seite behaupten, dass das Darlehen niedriger oder höher war, dass ein abweichender Zinssatz vereinbart wurde etc.. Grundsätzlich steht eine Finanzierungsgemeinschaft dem privaten Darlehen übrigens nicht entgegen. Der Freundes- und Familienkreis kann somit auch ein privates Funding anstreben. Auch hier gilt: Jeder Teilnehmer muss die Bedingungen schriftlich in den Vertrag einfügen. Im Privaten kann das so aussehen: Oma 5.000 Euro, Papa 1.000 Euro, Bruder 10.000 Euro etc. Alle müssen sich dann gemeinsam auf die Verzinsung und Raten einigen.

- Crowdfunding – auch diese Methode ist durchaus gängig, wobei es klar zwei Optionen gibt. Die erste, das echte Crowdfunding, besteht aus Privatpersonen als Geldgebern, die sich mit einer Summe an dem Vorhaben beteiligen können. Im Regelfall funktioniert dies gut, wenn das Unternehmen innovative Produkte vertreiben wird – die Geldgeber erhalten im Regelfall kein Geld zurück, sondern das Produkt. Die andere Alternative ist schon spezieller, denn hier investieren teils echte Investoren – auch mit hohen Beträgen. Sicherlich lässt sich viel regeln, doch meist erwarten die Investoren einen Anteil des Gewinns für ihre Ausgabe. Zugleich übernehmen sie einen gewissen Unternehmensteil. Allein die Suche über spezielle Plattformen unterscheidet sich von den ›echten‹ Investoren. Die zweite Form auch als Crowdinvesting bezeichnet.

- Investoren – vorab: Kein Investor gibt Geld für den guten Zweck, denn natürlich wollen sie an dem Unternehmen verdienen. Somit ist ein Businessplan wieder das Maß aller Dinge. Darüber hinaus muss jedoch auch die Chemie passen. Gerade zu Beginn steigen sogenannte „Business Angels“ gerne ein. Doch diese wollen neben einer reinen Kapitalspritze auch mit ihrem Know-how unterstützen. Aus diesem Grund ist es umso wichtiger, dass menschlich keine allzu großen Differenzen bestehen.

Vermutlich werden die meisten Gründungen mit einem Mix aus verschiedenen Finanzierungsquellen finalisiert. Schon das Eigenkapital setzt sich gerne aus verschiedenen Mitteln zusammen, die weiteren Gelder stammen aus Förderprogrammen, der Familie oder auch von Investoren. Wichtig ist, für alle Seiten einen guten Businessplan vorweisen zu können. Nur so gelingt im Normalfall auch der Pitch. Hierzu ein Beispiel: Wer ein spezielles Softwareunternehmen gründen will, welches eine spezielle Lösung für Hackangriffe anbietet, sollte diese Lösung in wenigen Sätzen klar verständlich präsentieren können.

Abbildung 2: Viele Wege führen zur gewünschten Finanzspritze. Gründer sollten alle Möglichkeiten sorgsam prüfen und am Ende eine informierte Entscheidung treffen. Bildquelle: @ Ibrahim Boran / Unsplash.com

Fazit – mehrere Wege führen zum Geldtopf

Gründer haben es sicherlich nicht leicht. Eine gute Idee allein bringt keine Einnahmen, denn erst mit der Umsetzung besteht ein Gewinnpotenzial. Doch Banken erwarten normalerweise genau das schon vorher: Finanzielle Sicherheiten. Dies macht es so schwer, an entsprechende finanzquellen zu gelangen. Dennoch gibt es durchaus Möglichkeiten und Wege, entsprechende Unternehmerkredite zu erhalten. Gerade die Gründerkredite der KfW oder die Gründungshilfen der Städte und Länder können hilfreich sein. Wer zugleich mit der Familie, dem Freundeskreis und vielleicht über das Crowdfunding Gelder generiert, der hat gute Chancen, tatsächlich das notwendige Kapital zusammenzubekommen.