Bzw. möchte ich doch wissen, wo das Geld in den Funktionsbereichen ausgegeben wurde? Marketing, Sales, Development, Betrieb, etc. oder?

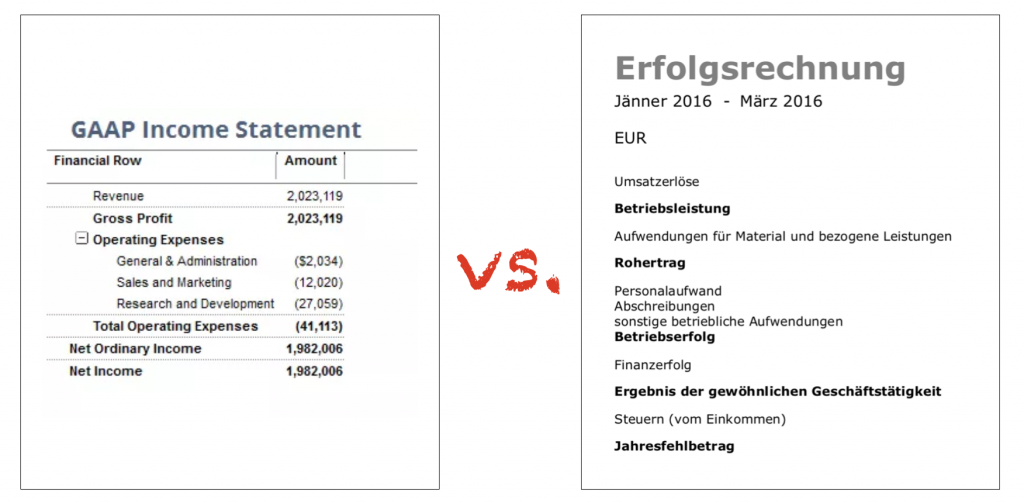

Gegenüber stehen zwei unterschiedliche Konzepte, die vor allem im Startup Bereich oft für Verwirrung und – aus unserer Sicht – zu zusätzlicher Komplexität und damit Kosten führen. Die hauptsächlich von internationalen Investoren bevorzugte Gliederung der Erfolgsrechnung (GuV) bzw. des Profit & Loss Statements (P&L) vs. der im deutschsprachigen Raum verwendeten Gliederung.

Bei Letzterem spricht man auch oft von der betriebswirtschaftlichen Auswertung (BWA). Jeder Unternehmer kennt diese, ist sie doch das vom Steuerberater bzw. Buchhalter regelmäßig übermittelte Berichtswesen. Eingeführt wurde dieser Begriff übrigens von DATEV im Jahr 1960 als DATEV-Standard-BWA-1. Heute wird die BWA von Banken auch als Instrument verwendet, um die Liquidität von Unternehmen zu bewerten.

Erstmalige vs. laufende Planung

Vor allem bei der Business Planung (von Startups) wird oft die Gliederung des GAAP verwendet. Warum? Weil viele Vorlagen im Internet diese Gliederung vorgeben und in den herunterladbaren Excel Vorlagen zu finden sind. Eine ausgezeichnete Vorlage von Christoph Janz von Point Nine Capital gibt es übrigens hier.

Für das Venture Unternehmen ist es praktisch, da damit international alle Pläne vergleichbarer und einfacher zu lesen werden. Bei der Erstellung vor allem des ersten Business Plans spielt die Gliederung eine untergeordnete Rolle. Die im GAAP oft extra aufgeführten Bereiche wie zB Administration (General & Administration oder kurz G&A), Sales & Marketing (S&M) und Research & Development (R&D) benötigen so oder so detaillierte Planannahmen, die dann in der Regel in eigenen Tabellenblättern in Excel ermittelt werden.

Spannender wird es, wenn der Business Plan dann zum Instrument für die Überwachung des operativen Betriebs oder zum Finanzierungsinstrument wird.

Der Steuerberater als Spielverderber

Und dann kommt die BWA vom Steuerberater. Und die passt aber so überhaupt nicht zu dem GAAP Business Plan. Nach mehr oder weniger langen Telefonaten ist dann auch klar: Der Steuerberater wird die Business Plan Gliederung NICHT abbilden. Aber so schwierig kann das doch nicht sein? Also beginnt man die manuelle Überleitung via Excel und schnell beschäftigt man sich einen halben Tag mit administrativen Aufgaben. Als ob es davon nicht schon genug geben würde!

Der Investor als kritischer Frager

Und dann steht eine Due Diligence an. Ein Investor möchte Einblick in das Unternehmen, bitte um Übermittlung des Business Plans und der laufenden Berichte des Steuerberaters. Der Quercheck bereitet aber Probleme, also landen Fragen auf dem Tisch des Unternehmers, die eigentlich nicht sein müssten und die wenig mit der eigentlichen Unternehmensvision zu tun haben. Im schlimmsten Fall geht Vertrauen verloren.

Die BWA als Allheilmittel?

Ist sie natürlich nicht. Aber aus Effizienzkriterien ist eine Planung auf Basis einer BWA sehr zu empfehlen. Man erhält dadurch ein geschlossenes Berichtssystem. Der Business Plan ist mit den monatlichen Berichten abstimmbar. Im Idealfall wird dieser Bericht vom Steuerberater mit eingepflegt. (Ist aber mit zusätzlichen Kosten verbunden.) Ausserdem kann einen Aktualisierung des Business Plans ganz einfach auch auf Basis historischer Zahlen erfolgen. Man sieht sofort den Verlauf von einzelnen Positionen über die letzten Monate oder Jahre und kann entsprechende Projektionen machen.

Aber ich möchte doch wissen, wo das Geld in den Funktionsbereichen ausgegeben wurde?

Schaut man sich die GAAP Gliederung genauer an, dann stellt man fest, dass die Funktionsbereiche oft lediglich die Personalkosten aufgliedern sowie zusätzlich leicht zu identifizierende und zuordenbare Aufwendungen. Sales & Marketing wären z.B. die Gehälter der Vertriebs- und Marketing Mitarbeiter sowie die Marketing Ausgaben. Die Marketing Ausgaben sind aber auch aus der BWA einfach ableitbar.

Eine “echte” Aufgliederung der Funktionsbereiche würde eine Kostenstellenrechnung (Cost Centers) erfordern. Diese ist aufwendig, teuer und betreuungsintensiv. Die Frage die hier jeder selbst beantworten muss lautet: Wieviel Information benötige ich wirklich und wieviel bin ich bereit, dafür an Geld oder Zeit zu investieren?

Und was kann man besser machen?

Aus unserer Sicht geht es in der laufenden Berichterstattung vor allem von klein- und mittelständischen Unternehmen (KMU) um die Beobachtung des Cash Flows. COMMITLY als Cash flow Planungs Tool hat daher die BWA mit einer indirekten Cashflow Ermittlung quasi verschmolzen. Wie COMMITLY den Cashflow ermittelt, kann man hier nachlesen.

Die Kategorien im Detail sind hier zu finden.