COMMITLY uses as a framework (template) for the Cash flow planning the so-called direct cash flow calculation. In financial jargon, this means that cash income is netted against cash expenses. In plain English, this means that we calculate the available cash flow or free cash flow as the difference between the incoming and outgoing payments on the accounts linked to COMMITLY.

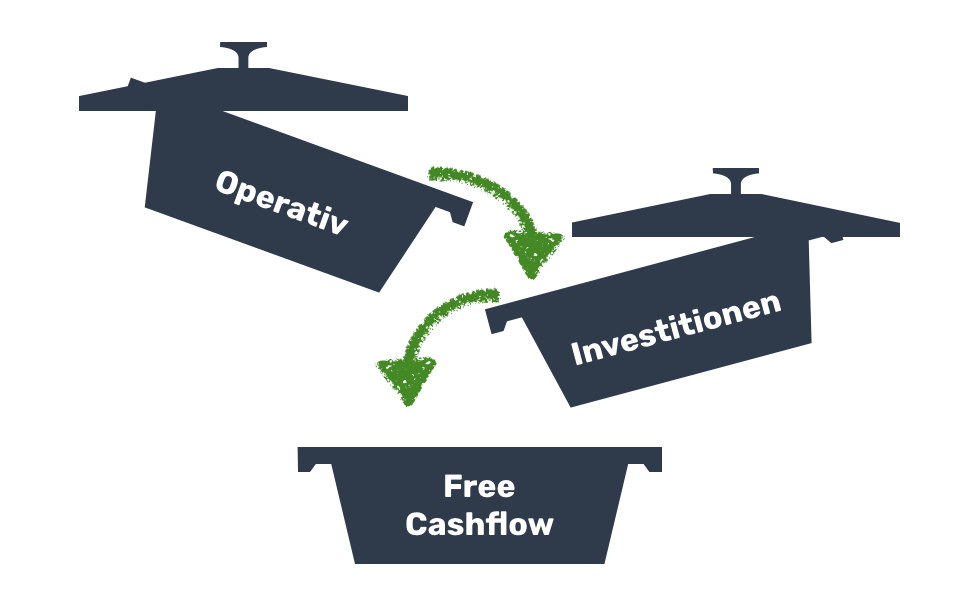

The scheme of direct cash flow determination

In the calculation, the inputs and outputs are divided into 3 groups:

A - Operating cash flow:

The operating cash flow indicates whether your business is able to finance itself. If the current income (incoming payments) is higher than your current expenditure (outgoing payments) in a certain period, everything is in the green. Keep it up!

B - Cash flow from investing activities

This pot indicates whether you have made investments or purchased assets for your business. If your cash flow from current business activities is positive, i.e. money is available or left over, you have the possibility to make investments, e.g. to buy a new workplace including a PC.

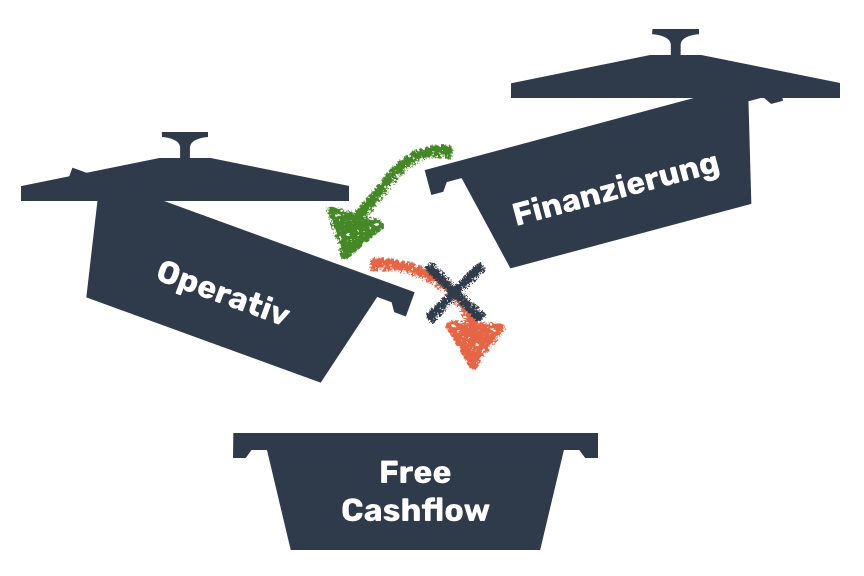

C - Cash flow from financing activities

This indicates whether your company has taken out or repaid loans or made payments to shareholders (dividends) or received payments from shareholders. A withdrawal in excess of the entrepreneur's salary also falls into this category. If the operating business activity does not provide enough cash flow, you can also make investments from this pot, e.g. with your business loan.

But why are these "pots" actually so important?

Because together they represent the financial strength of your company in the best possible way. We have shown the best case in our example: Your business is doing so well that you generate a surplus from your current income, can invest and even have something left over. By the way, what is left over is the "free cash flow".

A positive free cash flow / Free cash flow

The positive "free cash flow" is at your free disposal. This means that you have covered all current expenses, made investments and still have something left over. Congratulations!

What is the best thing to do with free cash flow?

- Build up a liquidity buffer as a precaution

- Invest in new projects or, for example, new employees

- Repaying loans early

- Remove profits

- ...

What to do in case of negative operating cash flow?

But what if your operating cash flow is negative, that is, if your expenses (outgoing payments) are higher than your income (incoming payments)?

Firstly, do not despair! Secondly: Keep in mind that you are not alone with this problem! Almost every entrepreneur knows this situation: In one month, the incoming payments are late and not all expenses can be paid smoothly.

Lucky who has built up a liquidity buffer from the previous periods. Then it is only a temporary liquidity shortage. If not, only cash flow from financing helps - i.e. reaching into one's own pockets or going to the investor or the bank.

So what measures can be taken?

- Check whether investments can be pushed backwards

- If there are realisable fixed assets, a sale (divestment) can possibly also be examined.

- Financing - is there access to loans, grants, fresh equity capital

- The waiver of withdrawals also falls within the scope of the financial return.

Is COMMITLY targeting the bank accounts exclusively?

The short answer is: Yes! And what about the data from accounting? The main task of accounting is the legally correct representation of the past. Planning concerns the future, has no legal requirements AND you can't "break" anything either. This is an important aspect that is also cited by our clients. The well-known investor Fred Wilson has also described another very important aspect in his blog - different types. The finance function: looking back and looking forward

"In my experience, the people who are strong in the look-back function are often not strong in the forward function. You may need different people to take on these roles. In a large company, there are very different departments that take on these functions. There's an accounting department and a financial planning department (often called FP&A)."

Does this mean that COMMITLY is only useful for revenue surplus calculators?

No! Companies with double-entry bookkeeping have only limited insight into their cash flow from the bookkeeping. This often leads to the indirect method being used to determine the cash flow. The starting point is the result for the period and so-called non-cash items, i.e. non-cash revenues and expenses such as depreciation, are deducted. In addition, there are issues with accruals and deferrals. However, the indirect derivation is so complicated that it is usually done by the tax advisor, with a corresponding time delay. BUT: A large tax consultant once told me that only 10% of HIS employees have any idea how to do it.

Isn't indirect determination better for larger companies after all?

Direct determination, as used by COMMITLY, is super simple and covers all scenarios and also accounting forms AND also company sizes. The "link", if you will, is the cash balance or the account balance of the banks. That is also what is special about COMMITLY. In practice, we have rarely (actually never) seen liquidity planning (and also cash flow reports) in Excel that could be reconciled 1:1 with accounting. COMMITLY guarantees that.

Why? Because at the end of a period, the most important basis of a tax advisor (whether EÜR or double-entry accounting) is the reconciliation with the bank account. And this is automatically guaranteed in COMMITLY.